Welcome to the Blog

Keep up with the latest news and updates

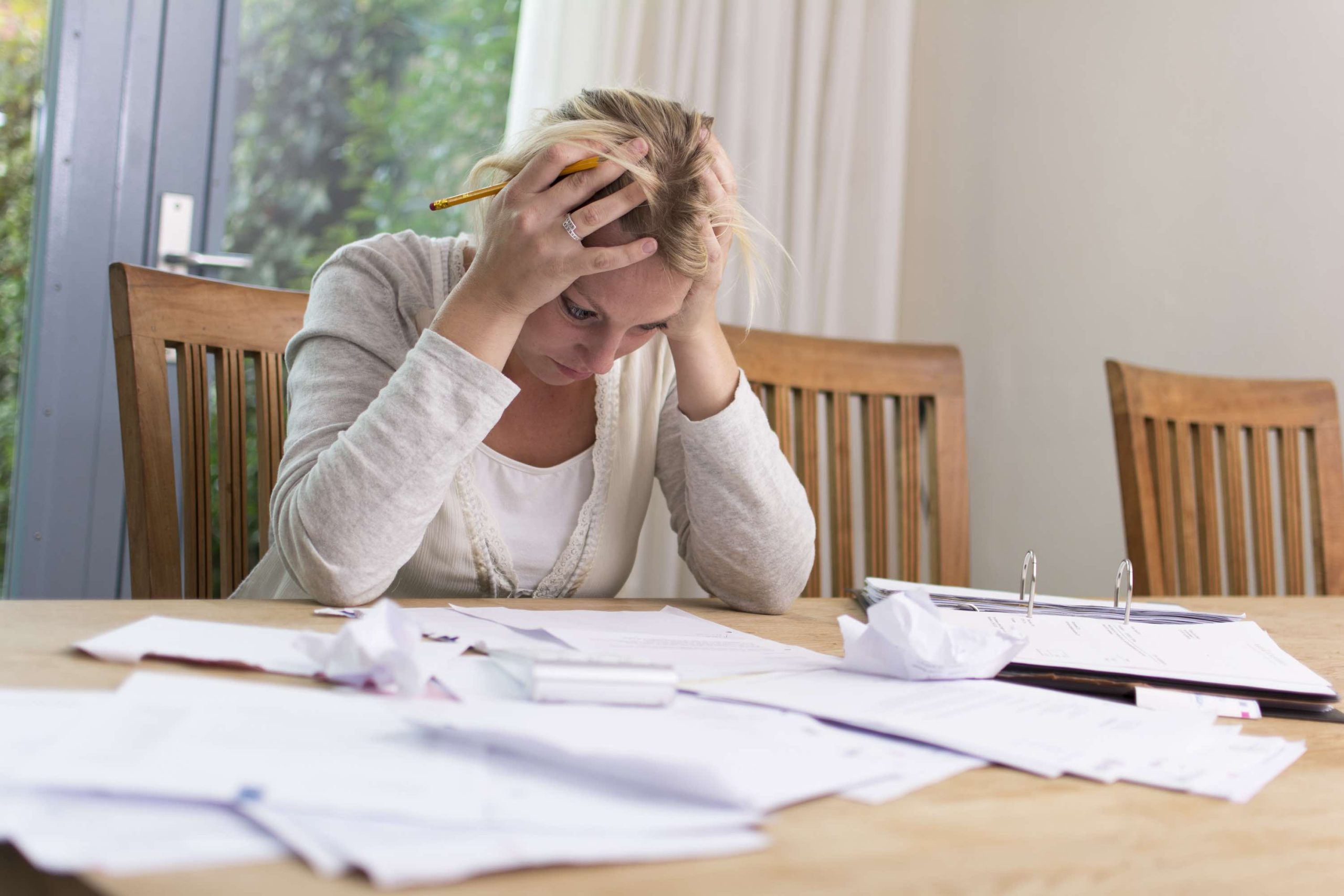

Maybe you’ve wondered about your own debt or perhaps your parent’s debt—what happens to that debt when you (or they) die? Well, it depends, and that’s part of the reason you want to ensure your estate plan is well prepared. How you handle your debt can greatly impact the people you love.

In some cases, you could inadvertently leave a reality in which your surviving heirs—your kids, parents, or others—are responsible for your debt. Alternatively, if you structure your affairs properly, your debt could die right along with you.

According to the Federal Trade Commission, an individual’s debt does not disappear once that person dies. Rather, the debt must either be paid out of the deceased’s estate or by a co-creditor. And that could be bad news for you or the people you love.

What exactly happens to this debt can vary. One of the purposes of the court process known as probate is to provide a time period for creditors to make a claim against the deceased’s estate, in which case debts would be paid before beneficiaries receive their inheritance. But if there is nothing in the probate estate and all assets are held outside of the probate estate, then what?

Well, that’s where we come in, and why it’s so important to get your affairs in order, even if you have a lot more debt than assets. Your “estate” isn’t just what you own, it includes what you owe, too. And with good planning, we can help you align it all in exactly the way you want.

Debt After Death

When an individual dies, someone will handle his or her affairs, and this person is known as an executor. The executor can either be someone of the individual’s choice, if he or she planned in advance, or someone appointed by the court in the absence of planning. The executor opens the probate process, during which the court recognizes any will that’s in place and formally appoints the executor to administer the deceased’s estate and distribute any outstanding assets to their loved ones.

During this process, the estate’s assets are used to pay any outstanding debt. This usually includes all of an individual’s assets, although it does not include assets with beneficiary designations, such as 401(k) plans and insurance policies. The estate does not own these assets, and they pass directly to the named beneficiaries. Given these factors, if an individual’s assets are subject to probate and the person has outstanding debt, their beneficiaries will receive a smaller share of anything left to them in the estate plan.

How Unsecured Debts Are Handled After Death

Typically, unsecured debts, such as credit card debts, are the last form of debt the estate repays. In most cases, the estate first repays any outstanding secured debts, including car and mortgage loans. Following this, the estate repays the legal and administrative fees associated with executing the deceased’s will. From there, the estate repays any outstanding unsecured debt, including credit card balances. Usually, if the estate lacks the assets to repay these debts, creditors have no choice but to accept the loss.

However, in some states, probate laws may dictate how the deceased’s creditors can clear these debts in other ways, such as by forcing the sale of the deceased’s property. It’s worth noting that there is a time limit for creditors to claim against an estate after the deceased dies, and this time frame varies between states.

Avoiding Probate

There are several things you can do to avoid probate. Perhaps the most common involves establishing a revocable living trust. Since the trust, not the estate, owns the assets, assets held by a properly funded and maintained trust do not have to go through the probate process.

Despite this, creating a living trust does not guarantee an individual’s assets will receive protection from creditors if that person has debt. What it does mean is that his or her heirs may have more flexibility compared to probate. In other words, by creating a living trust, your trustee may be able to negotiate with creditors more easily to reduce any outstanding debt. In theory, creditors may still sue to repay the debt in full. However, since this could involve significant costs, creditors may prefer to settle instead.

When Do Surviving Family Members Pay The Deceased’s Debts?

Most of the time, it’s unnecessary for surviving family members to pay the deceased’s debt with their own money. Instead, as noted above, payment of the debts are either paid out of the deceased’s estate, or if there is no estate, the debts are extinguished. However, there are some exceptions to this, including the following:

- Co-signing loans or credit cards: If someone cosigns a loan or credit card with the deceased, that individual is responsible for clearing any outstanding debt associated with that account.

- Having jointly owned property: If an individual has jointly owned property or bank accounts with the deceased, that person is responsible for clearing any outstanding balances associated with these assets.

- Community property: In some states, including California, Arizona, Nevada, Louisiana, Idaho, Texas, Washington, New Mexico, and Wisconsin, the surviving spouse is required to clear any outstanding debt associated with community property. Community property is any property jointly owned by a married couple.

- State laws: Some states require surviving family members, or the estate more generally, to clear any debts associated with the deceased’s healthcare costs. Additionally, if the estate’s executor failed to follow a state’s probate laws, it might be necessary for him or her to pay fines for doing so.

What To Do When Someone Dies With Debt

When someone dies with outstanding debt, it’s important to take swift action to handle their affairs and negotiate their debts. Below are some steps to follow when faced with this scenario:

- Understand Your RightsSince probate laws vary between states, it’s a good idea to thoroughly research the probate process in our state, or hire a lawyer to handle the estate for or with you. Many states require creditors to make claims within a specific period, while also requiring surviving family members to publicly declare the deceased’s death before creditors can collect any outstanding debt. It’s also against the law for creditors to use offensive or unfair tactics to collect outstanding credit debt from surviving family members. It’s generally a good idea to ask creditors for proof of any outstanding debt before paying.

- Collect DocumentsCollecting documents can be fairly straightforward, particularly if the deceased left all their vital financial papers in a single location. If the surviving family members cannot locate these documents, they can request the deceased’s credit report, which lists any accounts in the deceased’s name. As your Personal Family Lawyer®, we can do this for you, as part of our post-death support services.

- Cease Additional SpendingThis is essential to prevent any debts in the deceased’s name from increasing further, even if there is another person authorized to make payments. Ceasing additional spending. including canceling any recurring subscriptions, also helps prevent unnecessary complications when negotiating with creditors.

- Inform CreditorsProactively contact the deceased’s creditors to look into options for negotiating the debt, and notify credit bureaus of the death. To complete this process, it’s useful to have several copies of the death certificate to share with insurance companies and creditors. Afterwards, ask to close all accounts in the deceased’s name, and request the credit bureaus freeze the deceased’s credit, preventing others from unlawfully getting credit in his or her name.

- Close The EstateOnce all debt has been paid off, forgiven, or extinguished, the executor can officially close the estate. The process for doing this varies based on how assets and debts were held, so do not go into this part alone. Contact us to find out how we can support you.

We Can Help Ensure Your Family Doesn’t Get Stuck With Your Debt

Effective estate planning involves taking care of your affairs, and this includes ensuring your debts will be handled in such a way that your family isn’t left with a big mess or inadvertently forced into court. Consider scheduling a Family Wealth Planning Session with us, your Personal Family Lawyer® to determine how we can help protect your assets and prevent creditors from reducing the gifts you want to leave your loved ones after death. Contact us today to learn more.

Proper estate planning can keep your family out of conflict, out of court, and out of the public eye. Are you ready to protect your loved ones and legacy? Check out my next presentation.

What Happens To Your Debt When You Die?

If you are looking to create your last will and testament, or will, online, you’ll find dozens of websites that let you prepare a variety of estate planning documents for very little money, and even for free. With so many do-it-yourself online document services out there, you might believe you can create your will online, all on your own, without paying a lawyer to help.

And in some cases, you can create your will online.

But if you do, you need to understand how these services can backfire on you and your family. Online estate planning can be a catastrophe for those who aren’t aware of the risks. And as you’ll see, creating your will online without a lawyer’s guidance can even be worse for your family than if you’d done nothing at all.

Know what’s possible – and what’s not

A great way to start educating yourself is by watching this training video by family financial and legal expert Ali Katz. This free, one-hour training clarifies what you can do yourself online, and when you really need a lawyer’s support. The training also gives you access to an online tool you can use to create an inventory of all your assets, which is critically important to leave to your loved ones, no matter how much or little you have to pass on.

Meanwhile, if you are looking to create your own will online, first ask yourself the following 3 questions. After considering these 3 questions, if you determine you can create your own will online, you should seriously consider having us review it for you once you complete the document to be certain you’ve properly covered everything and everyone you care about.

1. Will your online will keep your family out of court?

When considering creating your own will online, the first question you need to ask yourself is: “Should I become incapacitated or when I die, do I want to keep my family out of court?” If your answer is “Yes, I 100% want to keep my family out of court,” then creating your own will online may not be the best idea.

While a will is a necessary element of most estate plans, it’s typically just one small part of an integrated plan. And a will by itself won’t keep your family out of court. In order for assets covered by your will to be transferred to your beneficiaries, your will must first pass through the court process known as probate.

During probate, the court oversees the administration of your estate and assets, ensuring your assets are distributed according to your wishes, while ensuring any creditors of your estate are paid, and managing any disputes that arise. Probate is lengthy, expensive, and open to the public, so you’ll want to have more than a will in place if you have any assets that would go through court in the event of your incapacity or death.

To avoid probate and keep your assets out of court, your will needs to be combined with other planning documents and important conversations as well, including a properly drafted and funded trust, up to date and effective beneficiary designations and conversations with family that ensure they won’t end up in conflict due to your lack of preparation.

Beneficiary designations and trust planning can be complex, and if you have assets that would otherwise pass through the court process, it may be difficult to ensure you are making all the right choices for your loved ones and your assets using an online document service. This is why we recommend that you begin your estate planning with a Family Wealth Planning Session, during which we can help you look at your family dynamics, and your assets, and assess what would happen to everything you have and everyone you love, when something happens to you. During this planning session, we can then determine the right plan for you and the people you love to help keep them out of court when something happens to you.

2. Is your online will’s execution legally valid?

If you do not have assets that would go through the court process, and you want to create an online will simply to name someone as your executor in the event of your death, you’ll want to make sure your online will is legally valid.

Each state has specific laws stipulating how a will must be documented and signed to be legally binding. If you fail to execute your will in accordance with these laws, the court can deem your will legally invalid.

If the court deems your will invalid, it’s as if the document never existed. In that case, a judge would name the person it considers is best to handle your estate, and your assets would be distributed according to state intestacy laws, which typically give priority to your closest living blood relatives.

If you want to ensure your online will is legally valid, you can look up your state’s laws governing the valid execution of a will. From there, make certain you sign it properly, with the right number and type of witnesses.

3. Does your online Will properly name an executor?

If you are going to create your own online will, the last question to consider is whether the will properly names an executor, along with back-up executors, and ensures that those you name will be appointed by the court in the event of your death.

An executor, also called a “personal representative,” is the person responsible for carrying out the instructions in your will. Your executor is typically named in your will and appointed by the court to locate and manage your assets, pay any outstanding debts and taxes you owe, and distribute your remaining assets to your beneficiaries.

If you don’t name an executor in your will, or the person you choose is determined to be unfit, the court will appoint an executor for you. As an example of how things can go wrong here, one common situation in which a named executor can be determined to be unfit is if your will does not waive the requirement for the executor to obtain a bond, and your named executor cannot qualify for a bond. This is a frequent mistake made by those who create their own will online.

If you’re unaware of these requirements when creating your online will, your chosen executor could be deemed unfit, leaving the choice up to the court. We can make certain your choice for executor is properly qualified, so you can rest easy knowing someone you know and trust will handle your final affairs and support your loved ones when you no longer can.

The Professional Support You Deserve

As you can see, creating your will online without a lawyer’s help is a huge gamble, and if you get it wrong, it can cost your family a lot more than money. Rather than relying on a one-size-fits-all document service, meet with us, your Personal Family Lawyer® to create your will and other estate planning documents.

Our Life & Legacy Planning Process is specifically designed to put in place the right combination of planning solutions to fit with your unique asset profile, family dynamics, budget, as well as your overall goals and desires. Until then, if you need to get your plan started or need us to review your existing documents, contact us today.

Proper estate planning can keep your family out of conflict, out of court, and out of the public eye. Are you ready to protect your loved ones and legacy? Check out my next presentation.

3 Essential Questions to Ask Before Creating Your Will Online

This week, before the year ends, consider these 5 financial, retirement and tax actions you may need to take before it’s either too late or very costly for your family. And, if you have living parents in their 70s, make sure you cover these considerations with them this week..

1. Review Your Investments to Harvest Losses

If you have investments in a taxable account (including cryptocurrency investments), you may want to consider selling off any losers to offset any gains you have made. Selling losses can help reduce your tax liability for the year, if you have any capital gains, and then you can carry forward investment losses to offset capital gains in the future.

If you are sitting with cryptocurrency losses that you haven’t recognized yet because you haven’t sold your cryptocurrency due to wanting to stay in the market for when crypto goes back up, you can have the best of both worlds. Sell your cryptocurrency now before the end of the year, and because the “wash sales” rules don’t apply to crypto tokens, you can buy the exact same tokens right back. In contrast, with non-crypto investments, you’d have to wait 30 days to buy back into the same investment, in order to harvest non-crypto losses.

Once the year 2022 ends, you can no longer harvest losses to offset against 2022 capital gains.

2. Contribute to a Retirement Account

If you have not yet reached your retirement account contribution limits for the year, you may want to consider contributing to a retirement account such as a 401(k) or traditional IRA.

Here are the contribution limits for 2022:

- 401(k), 403(b), and most other defined contribution plans: $19,500

- Traditional and Roth IRAs: $6,000 (plus an additional $1,000 catch-up contribution for those age 50 or older)

- SIMPLE IRA: $13,500 (plus an additional $3,000 catch-up contribution for those age 50 or older)

- SEP IRA: 25% of salary, up to a maximum of $58,000

3. Required minimum distributions (RMD) and qualified charitable distributions (QCD)

If you have a traditional IRA and you (or your parents) are age 73 or older, you (or they) need to take an RMD for 2022 by the end of the year.

If you are 72 in 2022, you have until April 1, 2023 to take your first RMD. Failing to take an RMD can result in a penalty of 50%. If you don’t need the income, consider converting your RMD into a qualified charitable distribution (QCD), which is a tax-free transfer directly from your IRA to a charity of your choice, up to $100,000 per year.

You must take RMDs or make a qualified charitable distribution by December 31, 2022, or you’ll pay the 50% penalty. Don’t miss this one.

4. Inherited IRA Required Minimum Distributions

If you inherited an IRA prior to the SECURE Act or if you are an eligible designated beneficiary who inherited in 2020 or 2021, you will need to take an RMD for this year. In addition, if you inherited an IRA this year, and the family member who left you that IRA did not take a required minimum distribution, you’ll need to take a year of death RMD this year, before the end of the year.

Note: The IRS has waived the 50% penalty for 2022 RMDs that are not taken when a beneficiary is subject to the 10-year payout rule under the SECURE Act due to confusion surrounding this new rule.

If you have an inherited IRA and you do not have a financial advisor, contact us to ask for our best recommendation for support.

5. ROTH IRA Conversion

If you are considering converting to a Roth IRA, now may be a good time to do so, as tax rates are currently low and markets have come down from their previous highs. You will need to act quickly, as the deadline for converting for 2022 is December 31.

This article is a service of a Personal Family Lawyer®. We do not just draft documents; we ensure you make informed and empowered decisions about life and death, for yourself and the people you love.

Proper estate planning can keep your family out of conflict, out of court, and out of the public eye. Are you ready to protect your loved ones and legacy? Check out my next presentation.

Checklist: 5 Financial Decisions to Consider Before December 31

The environmental costs of death are significant and constantly rising. With 8 billion people on the planet right now—all of whom have bodies that die and must be disposed of—we need to start seriously considering alternatives to traditional options for burial and cremation. Fortunately, more and more “green” options are being developed to reduce these costs, and this article looks at some of the latest innovations.

In most conventional burials, the body is pumped with toxic embalming fluid, placed in a steel casket, and buried within a cement-lined vault six-feet underground. According to the Green Burial Council, burials in the U.S. go through roughly 77,000 trees, 100,000 tons of steel, 1.5 million tons of concrete, and 4.3 million gallons of embalming fluid each year.

Although cremation is touted as more eco-friendly than burial, it still comes with serious environmental risks. In fact, cremating a single body uses about the same amount of gas as a 500-mile road trip, according to the Natural Death Center. Cremation also releases some 250 lbs. of carbon dioxide into the atmosphere, roughly the same amount an average American home produces in a week.

A Return To Nature

With the death rate expected to spike as Baby Boomers age, the funeral industry is poised to cause even more damage. While green funerals are a recent trend, natural burials were the norm until the Civil War, which coincided with the rise of the industrial age, embalming, and the modern funeral director business.

Today, natural burials are making a comeback. Green funerals are designed to not only be more environmentally friendly, but also less expensive overall than conventional burial or cremation. If you want to make your last act on this planet less harmful to the ecosystem, here are 6 green funeral options, along with the best way to include your final wishes in your estate plan.

1. Green burial

Founded in 2005, the nonprofit Green Burial Council (GBC) establishes environmental standards for green cemeteries, funeral professionals, and funeral-product manufacturers. According to the GBC, a green burial must meet three general criteria:

- The body cannot be embalmed.

- The body must be buried without a cement or metal vault or grave liner.

- Only biodegradable burial containers and shrouds may be used.

In green cemeteries, graves are typically marked by GPS or with a simple stone or tree, instead of headstones, metal plaques, and other ornate markers. The grounds are often planted with native species, forgoing pesticides and mechanical landscaping. The graves are shallower than conventional plots, exposing the body to more natural organisms to speed decomposition.

Green caskets are constructed from biodegradable materials, such as untreated wood, bamboo, wicker, or cardboard. Burial shrouds should be non-bleached, undyed, and made of natural fabrics like cotton, linen, silk, wool, or hemp. To find funeral providers in your area that offer green burial, use the GBC’s list of approved companies.

2. Aquamation

Without the need for embalming, caskets, or burial vaults, cremation is considered less harmful to the environment than burial. However, a new water-based method—aquamation—promises an even greener alternative. Also called “resomation” or “flameless cremation,” the method involves a chemical process in which lye, superheated water, and pressure dissolve the body, rather than burning fossil fuels. The ashes produced by aquamation can be scattered or placed in a biodegradable urn for burial.

3. Mushroom burial suits

One of the latest innovations in green funerals are special burial shrouds containing mushroom spores sewn into the fabric. The suit fits like long-john pajamas, and the mushrooms facilitate decomposition. In addition to absorbing and purifying toxins released by the body, the fungi delivers nutrients to the soil to encourage plant growth. When he died of a stroke at the age of 52, TV and film star Luke Perry was reportedly buried in a mushroom burial suit.

4. Eternal reefs

Eternal Reefs combine ashes from cremated remains with environmentally friendly concrete to create an artificial reef. Submerged on the ocean floor, these hollow “reef balls” create new habitats for coral, fish, and other marine life. Marked by GPS, your loved ones are encouraged to visit these living memorials by boat, snorkeling, or scuba diving. The company currently has locations in the waters off the following states: Florida, New York, North Carolina, Texas, South Carolina, Maryland, and New Jersey

5. Become a tree

If you aren’t near the water, but still want to leave a living memorial of yourself, a tree burial might be an attractive alternative. The startup Transcend plans to open forest-based cemeteries across the U.S., where rows of trees, rather than headstones, mark the graves. Here’s how it works: the body is wrapped in a biodegradable, linen shroud and placed in a shallow grave that’s lined with wood chips or hay. Then, a mixture of soil, wood chips, and fungi is used to fill the grave, and a young tree is planted on top. As the body decomposes, it provides nourishment to feed the tree.

Additionally, Transcend has partnered with the nonprofit One Tree Planted, which specializes in planting trees around the world. For every tree burial reserved, Transcend promises to plant an additional 1,000 trees right away. The company expects to launch their first tree burials in 2023. Visit their website to learn more, including how the company plans to ensure your tree will be well-maintained for years to come.

6. Human composting

Another way your death can create new life is by having your remains composted. Known as “human composting” or “recomposting,” the process is similar to composting used to fertilize gardens and farms. The body is first placed in a steel cylinder filled with wood chips, straw, and alfalfa, along with bacteria designed to break down organic matter.

After roughly a month, your body is transformed into what basically amounts to soil. The end product can either be returned to your family or used to revitalize local conservation areas. Developed in 2020 by the Seattle-based company Recompose, human composting is currently legal in five states: California, Washington, Oregon, Colorado, and Vermont, with legislation pending in Hawaii and Delaware.

Put Your Final Wishes In Your Estate Plan

Regardless of the method you select, it’s critical to include your desires, plans, and the money to pay for disposal of your body in your estate plan. While green funerals are typically less expensive than traditional burial and cremation, they can still cost thousands of dollars. To avoid burdening your loved ones, at the very least, your plan should include enough money to pay for your funeral and legally name the person you want to carry out your desired wishes.

Moreover, it’s typically not a good idea to leave money for your funeral in your Will. Any money left in your Will won’t be accessible to your family until your estate goes through the court process of probate, which can last months or even years. Since many funeral providers require full payment upfront, if you leave funds in your Will, your loved ones will likely be stuck with the bill.

To avoid the necessity for probate, we often advise our clients to leave money and directions for their immediate post-death wishes in a Revocable Living Trust. A Living Trust doesn’t require probate, so the money for your funeral would be available to your loved ones right away. In the terms of your Living Trust, you can specify how you want your funeral carried out, and the person you designate as Trustee is legally bound to use the funds in the exact manner the terms stipulate. This can be especially important for green funerals, which might not be something your loved ones would choose if left to plan things on their own.

Finally, you can change the terms of your Living Trust at any point during your lifetime, and with new alternatives being developed all the time, this flexibility would allow you to use the very latest innovations in green funerals. If you’re interested in creating a Trust to cover your funeral expenses, meet with us, your Personal Family Lawyer® to discuss the options.

Help Your Loved Ones And The Planet

With proper planning, you can ensure that your death is not only significantly easier and less expensive for your family, but that it also has the most beneficial impact on the environment. As your Personal Family Lawyer®, we will work with you to prepare an estate plan that includes enough funding to have your funeral handled in the exact manner you desire—without forcing your family to pay for it. Contact us today to learn more.

This article is a service of a Personal Family Lawyer®. We do not just draft documents; we ensure you make informed and empowered decisions about life and death, for yourself and the people you love.

Proper estate planning can keep your family out of conflict, out of court, and out of the public eye. Are you ready to protect your loved ones and legacy? Check out my next presentation.

Green Funerals: 6 Eco-Friendly Options For Your Remains

Whether it’s called “The Great Wealth Transfer,” “The Silver Tsunami,” or some other catchy sounding name, it’s a fact that a tremendous amount of wealth will pass from Baby Boomers to younger generations in the next few decades. In fact, it’s said to be the largest transfer of intergenerational wealth in history.

Because no one knows exactly how long aging Boomers will live or how much money they’ll spend before they pass on, it’s impossible to accurately predict just how much wealth will be transferred. However, studies suggest it’s somewhere between $30 and $90 trillion. Yes, that’s “trillion” with a “t.”

A blessing or a curse?

While most are talking about the many benefits the wealth transfer might have for younger generations and the economy, fewer are talking about the potential negative ramifications. Yet there’s plenty of evidence suggesting that many people, especially younger generations, are woefully unprepared to handle such an inheritance.

In fact, an Ohio State University study found that one third of people who received an inheritance had a negative savings within two years of getting the money. Another study by The Williams Group found that intergenerational wealth transfers often become a source of tension and conflict among family members, and 70% of such transfers fail by the time they reach the second generation.

Regardless of whether you’ll be the one passing on wealth or inheriting it, you must have a well-prepared estate plan in place to prevent the potentially disastrous losses and other negative outcomes such transfers can lead to. Without proper planning, the money and other assets that get passed on can easily become more of a curse than a blessing for you and your loved ones.

Proactive planning is the key

There are a number of proactive measures you can take to help reduce the risks posed by the coming wealth transfer. Beyond putting in place a comprehensive estate plan that’s regularly updated, openly discussing your values and legacy with your loved ones can be a key way to ensure your estate planning strategies work exactly as you intend. Here’s what we suggest:

1. Create your own estate plan

If you haven’t created your own estate plan yet—and far too many of you haven’t—it’s essential that you put a plan in place as soon as possible. It doesn’t matter how young you are, how much wealth you have, or if you have any children yet—all adults over age 18 should have some basic estate planning vehicles in place. If you have yet to get your estate plan started, meet with us, your Personal Family Lawyer® right away to get this crucial first step handled.

From there, be sure to regularly update your plan on an annual basis and immediately after major life events like marriage, births, deaths, inheritances, and divorce. Unlike traditional estate planning professionals, when you work with us, we maintain a relationship with you long after your initial estate planning documents are signed.

Indeed, our Life & Legacy Planning Process features proprietary systems designed to ensure your estate plan is regularly reviewed and updated over your lifetime, so you don’t need to worry about overlooking anything, as your family, the law, and your assets change over time. Be sure to ask about these systems during your visit.

2. Talk about wealth with your family early and often

Don’t put off talking about wealth with your family until you are in retirement or nearing death. As soon as possible, clearly communicate with your children, grandchildren, and other heirs what wealth means to you and how you’d like them to use the assets they inherit. Make such discussions a regular event, so you can address different aspects of wealth with your family as the younger generations grow and mature.

With everyone gathered under one roof for the holiday season, right now is the ideal time to have this discussion. If you feel anxious or uncomfortable talking about wealth with your family, reach out to us and ask for our help. As we covered in our previous article on how a recession can affect your family, we have processes and systems specifically designed to support you in having these delicate conversations, with far more ease than you trying to do everything on your own. We can even facilitate these discussions with your loved ones, if that’s something you are interested in.

And when you do have the conversation with your loved ones, focus the discussion on the values you want to instill, rather than what and how much they can expect to inherit. Let them know what values are most important to you, and try to mirror those values in your family life as much as possible. Whether it’s saving money, charitable giving, or community service, having your loved ones see you live your most important values is often the best way to ensure they carry those values on once you are no longer around.

3. Discuss your wealth’s purpose

Outside of clearly communicating your values, you should also discuss the specific purpose you want your wealth to serve in your loved ones’ lives. You worked hard to build your family wealth, so you’ve more than earned the right to stipulate how it gets used and managed when you’re gone. While you can add specific terms and conditions for your wealth’s future use in estate planning vehicles like Trusts, don’t make your loved ones wait until you’re dead to learn how you want their inheritance used.

If you want your wealth to be used to fund your children’s college education, provide the down payment on their first home, or invest for their retirement, tell them so. By discussing how you would like to see their inheritance used while you are still around, you can make certain your loved ones know why you made the estate planning decisions you did. And having these conversations now can greatly reduce future conflict and confusion among your family about what your true wishes really are when you are no longer able to explain your wishes.

A Trusted, Lifelong Guide For You And Your Family

No matter how much, or how little, wealth you plan to pass on—or stand to inherit—it’s critical that you take action now to make sure that wealth is secure and offers the maximum benefit to your family. As your Personal Family Lawyer®, our Life & Legacy Planning Process is designed to ensure the wealth that’s transferred is not only protected, but that it’s used by your loved ones in the very best way possible.

Moreover, every estate plan we create features a built-in legacy planning process, which ensures you can communicate your most treasured values, lessons, and life stories to those you leave behind. That’s why we call our services Life & Legacy Planning, not just estate planning. These intangible assets form the foundation of your family legacy, and they are often what we value most of all when it comes to our inheritance. Unfortunately, most estate planning lawyers focus little, if any, attention on such assets.

But we are not like most estate planning lawyers.

As your Personal Family Lawyer® firm, we will serve as your trusted, lifelong guide to ensure you make a lifetime of wise, forward-thinking choices for yourself and those you love most. And we will offer your loved ones the support they need to make the most important legal and financial decisions when you are no longer there to guide them. With our expert, caring counsel, you can rest easy knowing that the coming wealth transfer will offer you and your loved ones the most benefit possible, with the least amount of risk. Schedule your visit with us to get your Life & Legacy Plan started today.

This article is a service of a Personal Family Lawyer®. We do not just draft documents; we ensure you make informed and empowered decisions about life and death, for yourself and the people you love.

Proper estate planning can keep your family out of conflict, out of court, and out of the public eye. Are you ready to protect your loved ones and legacy? Check out my next presentation.

Will The Coming Wealth Transfer Be A Blessing Or A Curse For Your Family?

Although the end of the year can be a hectic time, it’s also the deadline for your family to implement a number of key tax-savings strategies. By taking action now, you can significantly reduce your tax bill due in April, but with just a few weeks left in 2022, you better act fast.

While there are dozens of potential tax breaks you may qualify for, here are 4 of the leading moves you can make to save big on your 2022 tax return. However, there may be other opportunities for saving, so meet with us, your Personal Family Lawyer® to make certain you haven’t missed a single one.

1. Maximize retirement account contributions

By maximizing your contributions to tax-deferred retirement accounts, such as IRAs and 401(k)s, you can not only save for retirement, but also reduce your taxable income for 2022.

In 2022, you can contribute up to $6,000 to an IRA and up to $20,500 to a 401(k) if you’re under 50, and up to $7,000 to an IRA and $27,000 to a 401(k) for those 50 and older. If you don’t have the cash available to fund the maximum amount, try to contribute at least any amount that will be matched by your employer, since that’s basically free money, and you lose it if you don’t use it.

That said, the ability to deduct your traditional IRA contributions from your taxes comes with certain limitations. These limitations are based on factors, such as whether or not you or your spouse is covered by a retirement plan at work and your adjusted gross income (AGI), so make sure you know how your family is affected by these limits when taking deductions. On the other hand, Roth IRA contributions are not tax deductible, since they are made after taxes are taken out, but withdrawals from a Roth in retirement are tax-free.

Additionally, consider maxing out contributions to your Health Savings Account (HSA). Contributions to HSAs for 2022 are capped at $3,650 for individuals and $7,300 for families, with an additional catch-up contribution of $1,000 allowed for those age 55 and older.

You have until December 31, 2022 to contribute to a 401(k) plan and until April 18, 2023 to contribute to an IRA or HSA for the 2022 tax year.

2. Defer income if you’ll make less next year

If you’re expecting to make significantly more income this year than in 2023, try to defer as much income into next year as possible. However, this strategy only makes sense if you’ll be in the same or a lower tax bracket next year.

This might mean asking your boss to delay paying a year-end bonus until after Jan. 1, 2023, or if you’re self-employed, waiting to invoice certain clients until the new year. On the other hand, if you think you’ll be in a higher tax bracket in 2023, you may want to do the opposite and accelerate income into 2022 to take advantage of a lower tax bracket.

Meet with us, your Personal Family Lawyer® to find out what’s best for your situation.

3. Use “loss harvesting” to offset capital gains

With the stock and crypto markets down this year, it can be the ideal time to use a strategy called “loss harvesting,” which means selling taxable investment assets, such as stocks, mutual funds, and bonds, at a loss to offset any capital gains you may have realized earlier in the year. Capital losses offset capital gains dollar for dollar.

If your losses exceed your gains, you can write off up to $3,000 of collective losses against other income. Any losses in excess of $3,000 can be carried over into the next year. In fact, you can carry over such losses year after year over your lifetime.

Note that the loss harvesting strategy does not apply to tax-advantaged accounts, such as 401(k)s, IRAs, and 529 plans. Additionally, the IRS “wash-sale” rule prohibits using this tax write-off for buying a “substantially identical” asset within a 30-day window before or after the sale that generated the loss.

Given the restrictions, you should always consult your CPA or financial advisor before employing loss harvesting to ensure it doesn’t backfire on you. And if you’d like us to meet with you and your CPA or financial advisor, we offer that service to the clients in our top-tier support plans, so be sure to ask about that if you’d love help getting all of your legal, insurance, financial, and tax systems organized and coordinated before the end of this year.

4. Watch your required minimum distributions (RMDs)—or ensure your parents are watching theirs—if you or they are over age 72

If you have an employer-sponsored retirement plan, including a 401(k), 403(b), traditional IRA, SEP IRA, or SIMPLE IRA, you must start taking required minimum distributions (RMDs) by April 1st of the year that follows the year you turn 72. After that, annual withdrawals must be made by December 31st each year to avoid a serious penalty.

If you fail to take the proper RMD, you may face a 50% excise tax on the amount you should have withdrawn based on your age, life expectancy, and your account balance at the beginning of the year. That said, if you do make a mistake, you may be able to avoid the penalty by requesting a waiver from the IRS. You can request a waiver if your failure to take the RMD is due to a reasonable error, and you take steps to make the required distribution. To request a waiver, submit Form 5329 to the IRS, with a statement explaining the error and the steps you are taking to correct it.

Note that in 2022 the IRS updated its uniform lifetime table to calculate RMDs to account for longer life expectancies. As a result, your RMDs for this year may be slightly lower compared to previous years. To determine your RMD, refer to the IRS RMD worksheet, or use an RMD calculator.

Maximize Your 2022 Tax Savings

Implementing these—and other—year-end tax-saving strategies could save your family thousands of dollars on your 2022 tax bill. But if you don’t act soon, some of these opportunities may vanish for good, so meet with us, your Personal Family Lawyer® today to schedule your appointment and lock in your savings.

This article is a service of a Personal Family Lawyer®. We do not just draft documents; we ensure you make informed and empowered decisions about life and death, for yourself and the people you love.

Proper estate planning can keep your family out of conflict, out of court, and out of the public eye. Are you ready to protect your loved ones and legacy? Check out my next presentation.

4 Year-End Tax-Saving Strategies For 2022

As you’ve surely heard by now, we’re in the midst of great economic shifts. The collapse of the crypto market, the roller coaster that is the stock market, rising interest rates, dropping home values, and inflation through the roof—it’s enough to make you sick. And it can make you sick unless you take the actions we are sharing here.

During every economic shift, whether it’s the Great Depression, the last Great Recession, or even during the pandemic, some people get rich, while others lose everything. Whether your family got rich, lost it all, or just hung on by their toes, you can learn from what happened and create the exact future reality you want for yourself and the people you love.

But to do that, you need to get into action now. In service to that, here are 3 steps you can take right away to change your family’s future and ensure you have the stability you need to sail through the economic shifts in the best way possible.

On that note, whether you’ll be passing on wealth or inheriting it, it’s crucial to have a plan in place to reduce the massive loss that will occur if you wait to start the estate planning conversation. Whether you have a little or a lot, not getting clear on what you do have (or will receive) can cause major upsets that can cost you far more than just money.

1. Get Into Conversation And Connection

The first step to ensure your family benefits from the current and coming economic shifts, regardless of what happens, is to get into conversation and connection with the people you depend on, the people who depend on you, or who you will depend on if something happens to you or your assets.

With the economic realities that are upon us, we can no longer go it alone, expecting everything to just work out because the stock market is on the rise and there’s plenty of savings cushion in the bank. Instead, this is the time to bring your family together and talk about what there is, where it is, and how it’s being managed (and will be managed) in the event there is a black swan event, such as the pandemic or a major stock-market crash.

If you are afraid to have these conversations because you think your family might not do well with knowing what you have, because you think they can’t handle knowing what you have (or don’t have), or because there has been upset in the past when talking about family financial resources, that’s a sign that it’s more important than ever to get into conversation and connection as soon as possible.

If you’ve attempted to have these conversations with your loved ones in the past and it hasn’t gone well, reach out and ask for our help. We’ve got processes and systems in place to support you to have these delicate conversations with your parents, kids, or siblings, with far more ease than you trying to do everything all on your own.

And if you don’t have living parents, kids, siblings, or a spouse, it’s even more important that you start these conversations. You can begin by identifying who you need to have these conversations with. We work with many single people and unmarried couples to help them navigate and talk about what can be a confusing and uncertain future, and we can help you, too.

If talking about assets and the allocation of family resources is easy for your family, that’s great—it’s time to take it to the next level by following the rest of the steps outlined here. Once you get into conversation with the right people based on your family dynamics, the next step is to get comfortable enough to “open the kimono.” This involves creating an inventory that lists all of the assets you own, where they are located, and how the people you love can find them in the event you become unable to share those details yourself.

2. Open The Kimono: Create Your “Family Wealth Inventory”

Whether you’ve created a formal set of estate planning documents already or not, it’s time to create (or update) an inventory of your assets. In our experience, most estate plans don’t do a very good job of keeping assets organized. When a loved one becomes incapacitated or dies, this is actually one of the biggest sources of expense, heartache, and pain—no one knows what there is, where it is, or how to find it.

One of the greatest gifts you can give the people you love is what we call a “Family Wealth Inventory,” and it’s something we create for all of our clients as part of their estate plan. We will not only create this inventory for you, but we have systems to keep it consistently updated year in and year out, as your life, assets, and the law change over time.

During a major economic shift, creating, updating, and revising your Family Wealth Inventory is critical, and doing that with the people you love is your number-one mission. As we see it, family wealth isn’t just about your financial wealth, it’s about your whole family’s wealth, including your intellectual, spiritual, and human assets. In fact, these non-financial, intangible assets are usually what we all care about most, and yet they are so often overlooked in estate planning.

One of the best ways to maximize your family’s intellectual, spiritual, and human assets is for your loved ones to get into relationships around your family’s financial resources. Begin by creating (or updating) your Family Wealth Inventory, and share it with your loved ones, so you can discuss how to best allocate (or re-allocate) those resources. Having this conversation can help ensure your family’s intellectual, spiritual, and human wealth continues to grow, even as we move through these uncertain economic times.

If you don’t have a Family Wealth Inventory yet, contact us and ask about our Personal Resource Map. This free, online resource-mapping tool will help you start creating your asset inventory right now, without the need for a lawyer. From there, meet with us for a Family Wealth Planning Session. During this meeting, we’ll look at what you have, where it is, and who will take care of it if you can’t, so we can create a plan that’s right for you and your family, whether we have a recession, depression, inflation, or whatever else may come our way.

3. Consider Reallocating Your Resources

Once you’ve created your Family Wealth Inventory, which allows you to see all of your assets in one place and consider the needs of your family, regardless of the economic climate, you may decide to reallocate your resources. For example, now might be the time to invest in multigenerational housing that will allow you and your kids to live together for many years or allow you to care for aging parents, while still maintaining privacy. Or you may decide that it’s time to create that homestead you’ve been talking about building, or launch that business you’ve been wanting to start. And it could be that now is the time to do all that with the people you love.

When we meet with you for a Family Wealth Planning Session, we’ll help you look at whether your resources are being held in ways that will support you to reach your short and long-term goals. Then, we can either help you reallocate your resources to achieve those goals, or refer you to professionals we trust to help you reallocate. The worst thing you can do right now is not looking at your family resources because you are afraid to see what’s there or you want to keep your head buried in the sand.

Times are changing, and the best time to look at what you have, so you can consider the future you want to create and intentionally allocate (or re-allocate) your resources is right now. Those who do so will thrive. Those who don’t will fall behind and wish they had done something different once it’s too late.

4. Update Your Plan

Once you look at what you have, where it is, and how you want it allocated, the next issue to decide on is who would take care of it all if you cannot. Leaving the management of your affairs to chance or to out-of-date estate planning documents is the worst thing you can do for yourself and those you love.

In an upcoming article, we’ll cover the Great Wealth Transfer that’s happening, detailing how between $30 and $80 trillion of wealth will be transferred between the generations over the next few decades, and how you can best prepare for that transfer.

In the meantime, start by updating the estate planning you already have in place to handle your assets in the event of your incapacity or death. If you don’t have any plan at all, the state has one for you, and it almost certainly isn’t what you would want to have happen. And if you do have an estate plan in place, it’s likely out of date, or possibly wasn’t even created properly, to begin with.

No matter what you have—or don’t have—we can help.

Secure Your Wealth, Your Legacy, And Your Family’s Future

Regardless of how much, or how little, wealth you own, now is the time to look at what you have, talk to your parents about what they have, and talk to your kids about what they’ll need to take care of you. And if you don’t have living parents or kids, talk to your siblings or close friends. As your Personal Family Lawyer®, our Life & Legacy Planning Process is designed to guide you to look at all of these things with ease and talk to the right people based on your family dynamics and assets, as affordably and effectively as possible.

Every plan we create has built-in support for your life and legacy, which can greatly facilitate your ability to make wise legal and financial decisions throughout your lifetime and beyond. That’s why we call our services Life and Legacy Planning, not just estate planning.

By working with us, as your Personal Family Lawyer®, you can rest assured that no matter what happens with the ongoing and future economic shifts, your family wealth will offer the maximum benefit for your loved ones. Schedule a Family Wealth Planning Session today to start having these critical conversations to ensure you and your family will thrive through the recession and any other calamity that may occur.

This article is a service of a Personal Family Lawyer®. We do not just draft documents; we ensure you make informed and empowered decisions about life and death, for yourself and the people you love.

Proper estate planning can keep your family out of conflict, out of court, and out of the public eye. Are you ready to protect your loved ones and legacy? Check out my next presentation.

How Will A Recession Affect Your Family?

If you earn a good living now, but you worry about not having enough money for a future time when you cannot work due to illness or injury, disability insurance is your answer. However, you need to make sure you are getting an insurance policy that will meet your needs and not waste your money. This article covers 7 issues to consider when purchasing disability insurance.

Disability Insurance: Issues to consider

The answers to these 7 questions can give you the best chance of finding a policy that is well-suited for your particular situation.

1. What is disability insurance?

Disability insurance pays benefits when you are unable to work because you are sick or injured. Most policies pay a benefit that replaces a percentage of your income. But disability insurance is not the same as health insurance—it will not cover your medical bills.

Instead, disability benefits replace a percentage of the income you lose due to your inability to work, so you can cover your basic financial needs, such as paying bills, covering daily living expenses, and providing for your family, until you can return to work. To begin your search for disability insurance, first you need to get clear about your minimum financial needs, or what we call your “minimum to thrive” number, should you become unable to work.

If you don’t currently know what your “minimum to thrive” number is, contact us for help calculating this number, and we can refer you to tools or an advisor who can support you.

2. Should I get disability coverage?

If you are the breadwinner in your family and your income would stop if you become ill or injured and could not work, you should look into disability insurance. According to U.S. government’s statistics, one in four 20-year-olds become disabled before reaching retirement age. Statistics like this make it all the more important that you consider protecting yourself and your family with disability coverage.

3. What’s the difference between short and long-term disability insurance?

There are two primary types of disability insurance: short-term and long-term. Short-term disability insurance typically lasts between 3 to 6 months, and sometimes up to a year or more. These policies generally cover about 60% to 80% of your monthly gross income, and the premiums you pay generally range from 1% to 3% of your annual income. One major upside to short-term policies is that payouts usually happen within two weeks, which can be a lifesaver in an emergency.

Long-term disability insurance can pay benefits for a few years or until your disability ends, even if that’s when you retire. Most long-term policies cover 40% to 60% of your monthly gross income, but policies that pay up to 70% do exist. Long-term disability policies also cost 1% to 3% of your yearly income, but based on the benefits, they tend to be more cost-effective in the long run.

That said, it can take up to 6 months to see a payout from a long-term policy, which may not be a realistic option if you need money immediately to cover your living expenses. Therefore, we recommend covering your short-term financial needs with emergency savings of 6 months, and then getting a long-term policy to cover your longer term needs.

4. What does ‘portability’ mean?

If you purchase your disability insurance through your workplace, ask if you can keep that insurance if you leave the company. If your insurance is non-portable, your coverage will end when you leave the job. Having a portable policy means that you will be covered no matter where you work.

Although many disability policies purchased through an employer are not portable, it’s definitely something you should look into. If portability is important to you, consider purchasing disability insurance on your own, rather than through your employer.

5. What are the renewal options for disability policies?

A “guaranteed renewal” policy allows you to renew, without making any changes to your coverage, but your premium can fluctuate. A “non-cancelable” policy means your coverage and your premiums cannot be changed, assuming you pay your premiums on time. Also, be sure to find out if premiums are waived during a qualified disability.

Given these considerations, the best policies will be non-cancelable and guaranteed renewable. Obviously, such policies will cost more, so consider what’s best for you, and if you need help making your decision, we’re happy to recommend a trusted insurance agent and then talk through the options with you.

6. How do cost of living benefits work?

Cost of living benefits are not included in most policies, but adding this rider is definitely something to consider. Cost of living benefits are designed to provide financial stability by offering an increasing benefit to keep pace with an increased cost of living, which is especially important right now, when we are experiencing unprecedented levels of inflation.

When choosing cost of living benefits, consider choosing policies that increase on a compounding basis. Compound interest is earned on the principal and the interest. This additional rider can help your benefits keep pace through inflation, even after your disability ends.

7. Do I need a ‘future increase’ rider?

A future increase rider is another option to consider adding to your disability coverage. It’s worth looking into particularly if you think your income may increase significantly over time. With this rider, you are able to increase the monthly benefit of your policy, regardless of your health status.

Without it, your policy will not change to protect your future income, and your benefits will pay out according to your income when you first obtained coverage. That said, many insurance companies will limit the total supplementary coverage that can be implemented each year with a future increase rider, so even if you have this option in place, the benefits might not fully reflect your future salary.

Get help choosing your coverage

When shopping for a policy, it’s best to work with an insurance agent who can survey many different companies to help you choose the right policy for your budget, age, health, and other factors. And remember, you must have the policy in place before something happens—if you’re already sick or injured, you can’t buy disability insurance to make up for lost income.

One of the ways we support our clients is by discussing matters like this with you during your Family Wealth Planning Session, or at your annual or 3-year review meetings after you’ve completed your Life & Legacy Plan with us. If you do not have an insurance agent you are already working with, we can connect you with an agent we trust, and then provide objective counsel to help you decide on the best coverage for you and the people you love.

If you are not already a client, contact us today to schedule your Family Wealth Planning Session. If you are, and you are ready for a review of your legal and financial choices, contact us for a plan review. We look forward to supporting your next step in Life & Legacy Planning.

This article is a service of a Personal Family Lawyer®. We do not just draft documents; we ensure you make informed and empowered decisions about life and death, for yourself and the people you love.

Proper estate planning can keep your family out of conflict, out of court, and out of the public eye. Are you ready to protect your loved ones and legacy? Check out my next presentation.

7 Issues to Consider When Purchasing Disability Insurance

If you have preferences about what happens to your digital footprint after your death, you need to take action. Otherwise, your online legacy will be determined for you—and not by you. If you have any online accounts, such as Gmail, Facebook, Instagram, LinkedIn, Apple, or Amazon, you have a digital legacy, and that legacy is yours to preserve or lose.

Following your death, unless you’ve planned ahead, some of your online accounts will survive indefinitely, while others automatically expire after a period of inactivity, and still others have specific processes that let you give family and friends the ability to access and posthumously manage your accounts.

In parts one and two of this series, we covered the processes that Facebook, Google, Instagram, Twitter, and Apple offer to manage your digital accounts following your death. Here in part three, we’ll conclude this series by covering the most effective methods for including digital assets in your estate plan.

5 Steps For Including Digital Assets In Your Estate Plan

If you’re like most people, you likely own numerous digital assets, some of which may have significant monetary value, and others which have purely sentimental value. You may even have some digital assets that you’d prefer your family not access at all when you pass away.

To ensure these assets are managed in exactly the way you want, take the following five steps to include this digital property in your estate plan. While many of these tasks you can do yourself, you’ll definitely want to consult with us, your local Personal Family Lawyer® to ensure your estate plan is properly prepared and works exactly as you intend.

1. Create A Detailed Asset Inventory, With Access Instructions

Start by creating a list of all digital assets you currently own. Then, for each asset, provide detailed information about where the asset is stored and how it can be accessed, including all of the relevant login information and passwords. If you have numerous different accounts, password manager programs, such as LastPass, can simplify this effort.

If you own cryptocurrency, it’s essential that you prepare detailed instructions about how to access it, and ensure that one or more people you trust are aware that you own crypto and know how to find your instructions. Additionally, accessing cryptocurrency often requires complex user identification data and private keys.

Moreover, to effectively manage these assets.the person you choose to control your crypto after your death will need to know how to use a variety of digital tools, such as online wallets, digital exchanges, and other programs. Given this, leaving a detailed “How To” guide can be an ideal way to ensure your loved ones can access your digital currency with minimal hassle.

After you’ve created your inventory and access instructions, store these documents in a secure location, with your other estate planning documents, and ensure your fiduciary (executor or trustee) and lawyer know how to access these documents should something happen to you. Finally, back up any digital assets stored in the cloud to a computer, flash drive, or other physical device to make them easier to manage. And remember to update your digital asset inventory regularly to account for any new digital property you acquire or accounts you close.

2. Add Your Digital Assets To Your Estate Plan

The next step is adding your digital assets to your estate plan. As with other assets, you’ll typically pass your digital property to your loved ones through either a will or a revocable living trust. Meet with us, your Personal Family Lawyer®, to determine which estate planning vehicles are best suited for your particular assets and situation.

From there, specify in your will or trust the person, or persons, you want to inherit each asset, and include detailed instructions for how you’d like each asset managed after your death, if that’s something you’re interested in. On the other hand, some assets might have no value to your family or be something you don’t want them to inherit or even access, so you should specify that those accounts be closed or deleted by your fiduciary.

One thing you should NEVER do is provide the account information, logins, or passwords in your planning documents, where others might read them. This is especially true for wills, which become part of the public record upon your death.

For maximum security, keep this sensitive information in a secure place, and let your fiduciary know how to find and use it. To make securing and managing your digital assets easier, consider using a digital management service, such as Directive Communication Systems, instead of trying to do everything yourself.

It’s also a good idea to include terms in your estate plan allowing your fiduciary to hire an IT consultant if necessary, especially if your fiduciary doesn’t have much technical experience, or if you have particularly valuable digital property. Having a consultant available can enhance your fiduciary’s ability to manage and troubleshoot any challenges that come up.

Alternatively, you can designate a separate co-fiduciary just to manage your digital assets. Known as a digital executor, this individual is specifically tasked with managing your digital assets upon your death. If you have a lot of digital property or you own highly encrypted digital assets, like cryptocurrency, this option can be an optimal solution for safeguarding your online property.

3. Limit Access

Your estate plan also needs to include instructions for your fiduciary about the specific level of access you want him or her to have. For example, do you want your executor or trustee to be able to read all your emails, texts, and social media posts before deleting them or passing them to your heirs?

If there are any assets you want to limit and/or restrict access to, we can help you add the necessary terms to your estate plan to ensure your wishes will be honored and your privacy protected.

4. Include Relevant Hardware

Your estate plan should also include provisions for passing on any physical devices—smartphones, computers, tablets, flash drives—on which your digital assets are stored. Having this equipment will make it easier for your fiduciary to manage your online assets. And since the data contained on such hardware can be wiped clean, you can even leave this gear to someone other than the person who inherits the data stored on the devices.

5. Check Service Providers’ Access Authorization Tools

Review the terms and conditions for each of your online accounts and web-based service providers for how they handle your data after death. As discussed in the first two parts of this series, some platforms have features allowing you to give your family and friends the ability to access, manage, and delete your accounts after your death.

If such functions are offered, use them to document the individual(s) you want to access and manage these accounts. Just make certain those you named to inherit your digital assets using the providers’ tools match the beneficiaries named in your estate plan. If not, the provider will probably give priority access to the person named with its tool, not your estate plan.

Adapt Your Estate Plan To The Evolving Digital Universe

As technology continues to evolve, it’s essential to adapt your estate plan to keep pace with these changes. As your Personal Family Lawyer®, we have the knowledge and experience to not only properly include your traditional assets in your estate plan, but all of your digital assets as well.

Indeed, we are keenly aware of just how valuable your digital property can be, and our Life & Legacy Planning Process is designed to ensure all of your assets—digital or otherwise—are protected, preserved, and passed on seamlessly to your loved ones in the event of your death or incapacity. Furthermore, we can ensure you have the maximum level of privacy, and you stay in full compliance with the latest laws governing the ever-changing digital universe. Contact us today to get started.

This article is a service of a Personal Family Lawyer®. We do not just draft documents; we ensure you make informed and empowered decisions about life and death, for yourself and the people you love.

Proper estate planning can keep your family out of conflict, out of court, and out of the public eye. Are you ready to protect your loved ones and legacy? Check out my next presentation.

.svg)