Welcome to the Blog

Keep up with the latest news and updates

What is it about celebrities that always draws us in? For whatever reason, we just can’t resist a good, juicy celebrity story. Maybe it’s because we can relate in some way, or maybe we feel like we can’t relate and that’s what makes celebrities interesting. Their lives always seem attractive but somehow… just out of reach.

So for the next few weeks, we’re going to look at the lives of 4 celebrities and see what we can learn from their stories. I think you’ll be surprised to learn that you have more in common with these folks than you thought (even if you don’t also have your own private jet).

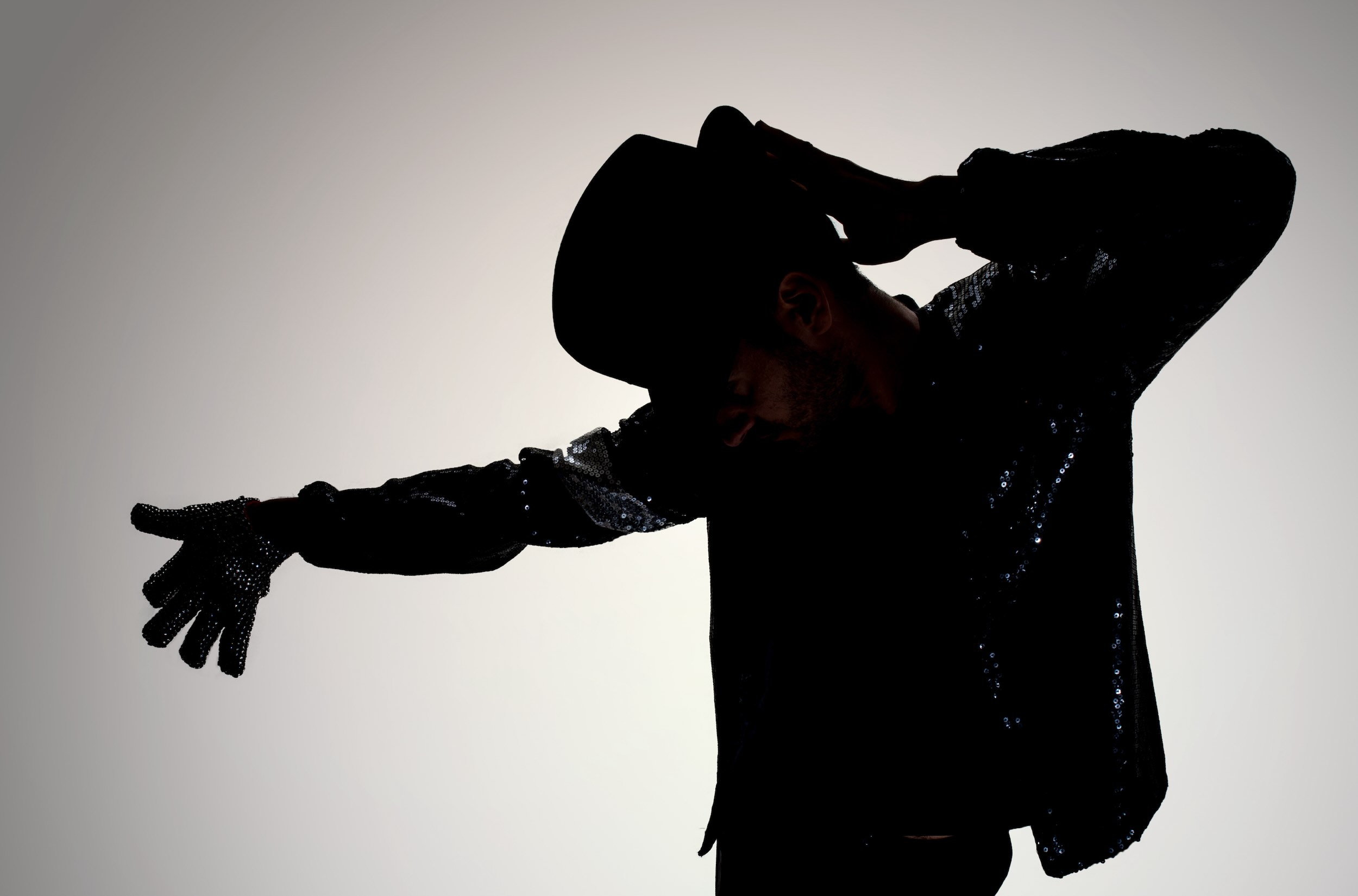

This week, we’re going to turn the spotlight on Michael Jackson. Even if you aren’t old enough to “Remember the Time” when Michael Jackson was dominating the charts, by the end of this article, you’ll see that he left holes in his estate plan that we can learn from.

Before we get started, however, I want to address the elephant in the room: many people, maybe you’re included, find Michael Jackson’s personal life and choices… concerning. That is completely understandable. The intent of this piece is not to defend or promote him in any way. Rather, this article’s focus is on his family and what they’ve endured in the court system for the last 15 years.

Now, let’s dive in and learn how you can avoid the same fate for your loved ones.

It’s As Easy as “ABC” (and 1, 2, 3)

Before we take a look at the specifics of Michael Jackson’s story, let’s dispel a myth about estate planning: That it’s only for the rich or philanthropic. You do not need to be rich, philanthropic, or famous to need estate planning. You need estate planning if you own anything – even a bank account – and have people in your life you love. It’s as simple as that (dare I say it’s as simple as “ABC” and 1,2,3?). So as you think about your own estate planning, it’s time to “Beat It” past the misconceptions so you’re empowered to do the right thing by your loved ones.

So what happened in Michael Jackson’s case? He had an estate plan that included a Will, and the Will established trusts for his mother, Katherine, and his three children, Paris, Prince, and Bigi.

Let’s stop right there because there’s already an increased potential for conflict with this setup.

When your assets pass via “Will” (instead of via Trust), your assets must go through a court process called probate, which, my mentor says, is a “lawsuit you file against yourself with your money for the benefit of your creditors.” Subjecting your assets and your family to probate can result in a long, time-consuming, and messy court process that can be unnecessarily expensive to resolve. Plus, the court process is entirely public, meaning anyone can access the records and see information about your assets and family that you would rather keep private.

A trust, on the other hand, bypasses the court process altogether, as long as your assets are owned in the name of the trust when you become incapacitated, or when you die. If your assets are properly transferred and retitled into the trust (this is called “funding” the trust), your estate can be administered privately and often takes less time than the court process does. A trust can be set up and funded while you’re alive, thereby avoiding probate, or it can be a part of your Will. When it’s part of your Will, like in MJ’s case, it isn’t established or funded until after the court process has played out. So if you’re trying to keep your family from going through the court process, putting a trust in your Will completely defeats the purpose.

Here’s what we’ve learned so far: if your intent is to keep your loved ones out of court and conflict, creating a Will alone is a “Bad” choice.

Peace of Mind For the “Man in the Mirror”

Since Michael Jackson’s assets were not owned in a trust, and instead his assets needed to pass via Will, there have been ongoing legal matters in court, which still aren’t resolved 15 years (yes, you read that right) after his death. Currently, MJ’s family is embroiled in a dispute with the IRS, and so the trusts he intended to be created for his mother and children remain unfunded, and therefore, some of his assets cannot be transferred to them, in the way it seems he intended. It’s also highly probable that the legal disputes continue to cost the estate a lot of money. That’s money that would have gone to his mother and children otherwise.

To make sure the people you love receive your assets in the way you want, I cannot underscore the importance of education and intent. This is exactly why my Life & Legacy Planning process begins with educating you first. The first time we meet, I will show you exactly what will happen to your family and your assets after your death, based on your current plan (or the state’s plan for you, if you don’t have a plan). From there, I help you make intentional decisions about what’s right for you and your loved ones, based on your desires, your assets, your family dynamics, and your budget.

Taxes – A Potentially “Dangerous” Situation!

The Jackson estate’s ongoing battle with the IRS also serves as a stark reminder of the tax implications that can affect your plan and your loved ones. When it comes to taxes, you can’t think in terms of “Black or White” – there are many shades of gray to consider. If you intend to avoid as many taxes as possible, you don’t want to cut corners by either doing your estate planning cheaply or on your own. That could be “Dangerous!” I can help you create a comprehensive plan that minimizes taxes as much as possible, potentially saving you and your family (lots of) money.

Speaking of saving money, taxes can significantly reduce the value of what you pass on to your heirs, which has a direct impact on your loved ones. To minimize this impact, together you and I will explore different strategies such as gifting assets during your lifetime, establishing irrevocable trusts, or using life insurance policies to cover potential tax liabilities.

So our next lesson from Michael Jackson’s story is: when it comes to saving money on taxes, the stakes are too high to go at it alone. Work with a professional who can advise you properly. We aren’t clear why Michael Jackson didn’t get the kind of support necessary to minimize taxes and protect his estate from a long drawn-out court process, but what we do know for sure is that we can help you and your loved ones.

Avoiding the “Thriller” of Legal Disputes

The Jackson case also highlights the importance of choosing the right representatives for your estate. These are the people who handle your affairs after you’re gone (they’re called “executors” if there’s a Will or “trustees” if there’s a Trust). MJ’s family members have criticized the representatives for the way they’ve managed the estate. In particular, Katherine Jackson has alleged that the executors have been too frugal and are holding onto assets to maintain control.

There’s always a possibility of conflict between your representatives and your loved ones, even if you aren’t famous and don’t have millions of dollars to fight over. So to help minimize the potential, we recommend you communicate your intentions to your representatives and to your loved ones during your lifetime. Consider holding a meeting so everyone knows what your wishes are and understands the intent behind your decisions. You may not be able to “Heal the World” on your own, but you can promote healing within your own family and prevent future conflict by opening the lines of communication now. We often facilitate these meetings for our clients.

Also, know that you don’t have to choose family members to be your representatives – even if you feel pressured to do so. If you aren’t sure who the “right people” are, think about people you know who are not only trustworthy but also capable of handling complex financial and legal matters. There’s also the option of choosing a professional representative, as Michael Jackson did, who might be more appropriate for your situation. When you work with us, we’ll be there to “Rock With You” through all the different scenarios that could arise, so you can then choose the right people for your unique circumstances.

Our two final lessons from Michael Jackson’s story are these: 1) Communicate your wishes openly to your representatives and your family, and 2) Choose the right people to act for you when you no longer can.

By learning from the challenges faced by Michael Jackson’s family, you can ward off the possibility of a similar outcome for your loved ones. Your careful planning today can pave the way for a smoother transition of your assets in the future, ensuring that you are able to support your family after you’re gone, rather than creating a mess for them to handle without you. I’m here to serve you and help you ensure your estate doesn’t become a “Thriller” of legal battles, but instead a harmonious transition that would make even the King of Pop proud.

“You Are Not Alone” – We’re Here for You

It’s “Human Nature ” to want to avoid thinking about your death, much less plan for it. We get it. But when we face our mortality, we’re able to live a more fulfilling life. The good news is that you don’t have to deal with it alone. We’re here to support you every step of the way.

As a Personal Family Lawyer Firm, we help you create a Life & Legacy Plan from a place of education and intention, so that your loved ones stay out of court and conflict. And once you’ve created your plan, you can rest easy knowing your wishes will be honored, your loved ones cared for, and your legacy preserved.

Click here to schedule a complimentary 15-minute consultation to learn more:

This article is a service of a Personal Family Lawyer® Firm. We don’t just draft documents; we ensure you make informed and empowered decisions about life and death, for yourself and the people you love. That’s why we offer a Life & Legacy Planning Session™, during which you will get more financially organized than you’ve ever been before and make all the best choices for the people you love. You can begin by calling our office today to schedule a Life & Legacy Planning Session™.

The content is sourced from Personal Family Lawyer® for use by Personal Family Lawyer® firms, a source believed to be providing accurate information. This material was created for educational and informational purposes only and is not intended as ERISA, tax, legal, or investment advice. If you are seeking legal advice specific to your needs, such advice services must be obtained on your own separate from this educational material.

Proper estate planning can keep your family out of conflict, out of court, and out of the public eye. Are you ready to protect your loved ones and legacy? Check out my next presentation.

Celebrity Estate Plans Series Part 1 of 4: Michael Jackson

As you celebrate the Fourth of July and all it represents – freedom, independence, and the pursuit of happiness – take pride in the ultimate American liberty: the right to decide your own affairs, even after death or in the event of incapacity. An estate plan, specifically a Life & Legacy Plan, is the way to express your liberty. It’s your personal Declaration of Independence. I know; it sounds weird. How in the world can an estate plan give me freedom?

Here’s how: Creating a Life & Legacy Plan (a unique estate planning process I use in my firm) preserves your self-determination, protects your family, grows your wealth, and defines your legacy on your own terms. Just as the Founding Fathers declared freedom from the British crown over two centuries ago, your Life & Legacy Plan declares your autonomy from the courts, state laws, and conflicting viewpoints that could unravel your final intentions. Read on to find out how.

You Have a Plan: It Just May Not Be What You Want

The first thing to know is that you already have a plan for what happens in the event you become incapacitated or when you die. You may not know what that plan is, and you may not like what that plan is! You see, the government has created a plan for you, without your input. Or, you may have already created your own plan, but didn’t really understand the choices you made, haven’t updated it, or may not even own your assets in a way that has them covered by your plan.

When you have a Life & Legacy Plan, you get to override the government’s plan for you with your choices. YOU get to decide exactly how you want your assets collected and distributed – whether that’s providing for certain loved ones over others, leaving assets to chosen family members, who aren’t related by blood or marriage, but who have become close kin to you by choice, or donating portions to charitable causes near and dear to your heart.

With a Life & Legacy Plan in place, you maintain that plan throughout your lifetime, so as your assets change, your life changes, and the law changes, so does your plan. It grows with you, rather than becomes stale and outdated over time. Because you aren’t a stagnant human. You are evolving, changing and likely growing. Your plan needs to evolve, change and grow along with you, otherwise it’s not even worth the paper it’s written on.

The Liberation of Making Your Decisions With Eyes Wide Open

Planning for incapacity or death is the equivalent of planning for your best possible life, and for the best possible life of the people you love. It may not have ever been presented to you that way, but think about it – if you accept that you are going to die one day, and you may become incapacitated first, and you want your family and assets to be cared for in a certain way when those things happen, wouldn’t that naturally inform choices you’ll make around the allocation of your resources throughout your life?

We call this “eyes wide open” decision-making, and it leads to the most optimal use and allocation of your resources throughout your life, and makes things as easy as possible for the people you love, in the event of your incapacity or death. For example, when you consider how you want to be cared for in the event of your incapacity, and document those choices, you can then ensure you have the necessary close personal relationships to deliver on your desires, as well as the required financial means to provide for yourself or the people who will care for you (or your kids). Otherwise, you are just leaving it up to happenstance … or a judge … and we call that “eyes squeezed shut/pretend it’s not going to occur” decision-making, and it’s not responsible, mature or kind to yourself or the people you love.

The Power to Choose

The most mature, adult and loving thing you can do for yourself and the people you love is to clarify well in advance how you want to be cared for, if you cannot care for yourself, who should make decisions for you, and how you want those decisions to be made. In addition, it’s critical to provide a roadmap for the people you love, so they know what you have, where it is and how to find it.

Establishing a Life & Legacy Plan does all of that, and it doesn’t matter how much or how little you have because your loved ones will have to deal with it, whether it’s a little or a lot — and your choices while you are living, healthy and clear empowers them and minimizes their outlay of time, energy and attention they may not have, especially during a time of grief. With a Life & Legacy Plan we help you create, you can also account for special circumstances like children or spouses from previous marriages, loved ones with disabilities, or family members you intentionally want to omit. No more worries about assets getting unfairly split or ending up in the wrong hands.

Finally, holding a family meeting can unite your loved ones around a shared understanding of your intentions rather than driving them apart through conflicts and differing interpretations of your wishes. Your Life & Legacy Plan gives you the power to choose to create more ease for yourself and the people you love.

A Declaration of How You Want to Be Remembered

Your Life & Legacy Plan represents your final declaration of the values and life experiences you’ll impart to loved ones and the world at large. Use this opportunity to put your final stamp on how you want your individuality and life’s purpose remembered, rather than leaving it up to chance, or leaving a legacy of mess and drama.

All of our plans include a Life & Legacy recording that guides you to express your deepest hopes, guiding wisdom, and ethical frameworks acquired over decades of successes, struggles, and personal growth. You will share cherished stories, meaningful quotes, and carefully-cultivated philosophies that give your life meaning. The Life & Legacy recording is the most meaningful gift your family will cherish and carry into future generations.

So, this Independence Day, make your own personal declaration of freedom by establishing your own comprehensive Life & Legacy Plan. Take pride in exercising your liberties to the fullest by removing all uncertainties over your final affairs and ensuring your true wishes will be honored.

Let Us Be Your Life & Legacy Planning Partner

As a Personal Family Lawyer Firm, Life & Legacy Planning is all we do. We work with you to craft a plan on your terms, taking into account what you want, not what someone else has decided for you. And once you’ve created your plan, you can rest easy knowing your wishes will be honored, your loved ones cared for, and your legacy preserved.

Contact us to learn more about how we help you exercise freedom over your own choices. Click here to schedule a consultation.

This article is a service of a Personal Family Lawyer® Firm. We don’t just draft documents; we ensure you make informed and empowered decisions about life and death, for yourself and the people you love. That’s why we offer a Life & Legacy Planning Session™, during which you will get more financially organized than you’ve ever been before and make all the best choices for the people you love. You can begin by calling our office today to schedule a Life & Legacy Planning Session™.

The content is sourced from Personal Family Lawyer® for use by Personal Family Lawyer® firms, a source believed to be providing accurate information. This material was created for educational and informational purposes only and is not intended as ERISA, tax, legal, or investment advice. If you are seeking legal advice specific to your needs, such advice services must be obtained on your own separate from this educational material.

Proper estate planning can keep your family out of conflict, out of court, and out of the public eye. Are you ready to protect your loved ones and legacy? Check out my next presentation.

Value Freedom? Here’s Why an Estate Plan Is Your Declaration of Independence

June marks Men’s Health Month, a time dedicated to raising awareness about health issues predominantly affecting men and encouraging the early detection and treatment of disease among men and boys. So this month, let’s turn the focus to you, gentlemen. You already know that taking care of your health allows you to prolong your life and enhance your quality of life. But have you given serious thought to how your health directly impacts your future? Your legacy? The ones you love the most?

What we’re talking about here is estate planning, and it’s every bit as important as your physical health. I know, I know, it could sound weird to equate health with estate planning, but hear me out. By the end of the article, the connection will be clear.

The Link Between Your Health and Estate Planning

Estate planning often brings to mind wills, trusts, and other legal paperwork, and in fact, that’s maybe what you initially thought when you read the title of this article. However, I want to challenge that assumption with this: the documents are merely the byproduct of estate planning.

You may be thinking, How are documents the “byproduct” of estate planning? Here’s what I mean.

Estate planning is all about ensuring your wishes are honored if you become incapacitated so you can live and die with dignity. It’s also about ensuring that the people you love most will know you loved them, that they’re cared for when you’re gone in a way you cared for them while you lived, and that you’ve removed all the pain, potential conflict and expense they will have to endure if you have no plan in place. Estate planning supports your loved ones to grieve in peace rather than face a long, expensive court process or confusion regarding how to find your assets or understand what to do when you are gone.

Estate planning is also about leaving a legacy. Contrary to what you may be thinking – that legacy is not only related to money and reserved for the wealthy and philanthropic – legacy is about the mark you make on those you hold most dear. It’s about defining your humanity and what you stood for. Putting your affairs in order now so your loved ones don’t have to deal with a mess later is a legacy, too. Making it clear that you loved your family is a legacy.

What about health? How does your health connect with estate planning?

Your health plays a significant role in shaping your preparations for the future in general, and how you structure your estate plan in particular. I want to first say that while “health” can refer to mental health, emotional health and spiritual health, and all are important, we’ll focus on physical health here.

So let’s take a look at the direct link between your physical health and estate planning. You’ll come to see that by prioritizing your physical health, you can not only enjoy life with more ease, but also avoid complications in your estate planning.

Longevity and Retirement Savings. Your physical health has a direct impact on your lifespan, which in turn affects how long your retirement savings need to last. If you maintain good physical health, you’re likely to live longer (yay!) and will need a more extensive plan regarding your assets, for your longer life.

Healthcare Decisions. Consider the potential need for long-term care. Alzheimer’s or dementia could require long-term care solutions that you may or may not choose. In your estate plan, it’s crucial to not only make sure you’re financially covered for these possibilities, but to also ensure you’ve made it clear how you want to be cared for, if you cannot make decisions for yourself. There comes a point in time at which it’s too late for you to make your wishes known, and given that you are reading this … now is the time to document what you would choose, if you could not choose.

This is why you need a healthcare power of attorney or a living will in your plan. These are documents that designate the person (or people) you choose to make medical decisions on your behalf if you’re unable to do so. Your designated healthcare agent (or agents) will not only ensure that your healthcare preferences are respected but will also align your medical treatment with your personal wishes. Without these documents in place, a judge (i.e., a complete stranger) could appoint someone to act on your behalf. Maybe even someone you don’t trust or wouldn’t want making decisions for you. Or, in a worst case scenario, a judge could even appoint a professional conservator who could drain your estate financially.

Disability and Its Impact. Poor health can sometimes lead to disability, affecting your ability to manage your own affairs. Including a disability clause in your estate plan ensures that your assets are managed according to your wishes, even if you’re not able to oversee them personally. A revocable living trust can be particularly useful here, as it allows your chosen person or entity to manage your affairs without the need for court intervention. Again, without a plan in place, a judge will make decisions for you, and those decisions may not be what you want.

Having gone through the potential consequences of not prioritizing your physical health and its direct link to your estate planning, let’s turn to practical steps you can take now to make sure you and your family don’t have to experience any negative consequences.

Practical Steps to Integrate Health and Estate Planning

Unless you’re already incapacitated and can’t make decisions for yourself, know that it’s not too late to take action. It’s not too early, either. Death and incapacity don’t discriminate based on age. When you face that fact, and then plan accordingly, you can live life with more ease, more joy, and less stress. Truly.

So if you haven’t planned for the future, here are some practical steps you can take now:

Schedule Regular Check-Ups. It may seem obvious, but regular medical examinations are vital. They not only help in detecting illnesses early but also provide a clear picture of your health, which, as we’ve discussed above, is crucial for accurate estate planning. If you discover a new health condition, you can plan accordingly when you’ve caught it in time. If not, it could be too late to get your plan in place.

Update Your Estate Plan Regularly: As your health changes, so should your estate plan. Make it a habit to review and update your plan on a regular basis or whenever there is a significant change in your health. As a Personal Family Lawyer®, I can not only help you get your initial plan in place, but with a unique process I use called Life & Legacy Planning®, I will always include a free review of your plan at least every three years. This ensures your plan works because it will be updated as your health, life and assets change over time. Without updates, your plan will fail, sending your family to court and increasing the probability of conflict.

Discuss Your Plans Openly: Talk with your family about your healthcare wishes and how they relate to your estate plan. Taking this courageous, and maybe uncomfortable, step, makes a big difference when it comes to decreasing the likelihood of conflict in your family. Make sure to discuss your preferences for end-of-life care, which can create conflict in your family if you haven’t clarified your wishes.

Consult A Professional Who Has Your Best Interests in Mind: I approach estate planning from a place of heart, always keeping your best interests, and by extension, your loved ones’ best interests, in mind. I not only help you to get your plan in place, but also help you keep your family out of court and conflict so your legacy is one of love and care. I can also help you navigate difficult discussions with your family about your wishes, so you can feel confident knowing you’ve done all you can to preserve the family bonds.

How We Support You and Your Loved Ones

As a Personal Family Lawyer® Firm, we recognize the integral connection between your physical health and your estate planning needs. Our commitment goes beyond mere legal documentation; we aim to ensure your life’s work and values are preserved with dignity and clarity. By understanding the specific challenges and opportunities that arise from your health, we tailor estate plans that not only protect your assets but also your well-being and your family’s future.

This Men’s Health Month, take a proactive step toward safeguarding your legacy and enhancing your peace of mind. Contact us to learn how our Life & Legacy Planning® process can align your health priorities with your estate planning goals. Click here to schedule a 15-minute consultation to discuss your next best steps:

This article is a service of a Personal Family Lawyer® Firm. We don’t just draft documents; we ensure you make informed and empowered decisions about life and death, for yourself and the people you love. That’s why we offer a Life & Legacy Planning® Session, during which you will get more financially organized than you’ve ever been before and make all the best choices for the people you love. You can begin by calling our office today to schedule a Life & Legacy Planning Session.

The content is sourced from Personal Family Lawyer® for use by Personal Family Lawyer firms, a source believed to be providing accurate information. This material was created for educational and informational purposes only and is not intended as ERISA, tax, legal, or investment advice. If you are seeking legal advice specific to your needs, such advice services must be obtained on your own separate from this educational material.

Proper estate planning can keep your family out of conflict, out of court, and out of the public eye. Are you ready to protect your loved ones and legacy? Check out my next presentation.

The Surprising Connection Between Men’s Health and Estate Planning

When your child turns 18, they’re legally considered an adult even though they have a lot more growing to do (though they may not think so!). Just like any other adult, their health and financial information is protected by privacy laws. But unlike any other adult, that’s still your child and you want to be there to support them in a crisis. Unless you’ve planned ahead you won’t be able to step in and support your child.

As an estate planning attorney, I often see families caught off guard when I tell them this. Like those families, you may also assume that as a parent, you’ll always have a say in your child’s medical and financial matters. But you don’t. Under the law, you have just as much access to their medical and financial information as you do for Joe down the street (which is none).

The good news is that with proper planning, you can help your newly-minted adult child navigate this transition and ensure you’re able to step in if something happens. Here I’ll share 3 strategies to help you and your child make the transition to their adulthood as easy as possible.

Strategy 1: Education

The first strategy for a successful transition to adulthood is education. At my firm, I start every client relationship with education. That’s because I believe that education equals empowerment, which supports you to make the right choices for yourself and your family. Young adults also need to be empowered through education. The more you can teach your child about their new financial and legal responsibilities, the more empowered they’ll be to make the right decisions.

If you haven’t already started talking with them about legal and financial matters, now is the time s. Start with a kind of budgeting we call “money mapping”. Explain the importance of tracking their income and expenses, setting financial goals, and investing wisely, both now and for the future.

Help them understand the basics of banking, such as how to use checking and savings accounts, the benefits of maintaining a good credit score, and assist them in setting up their own bank account if they don’t already have one. Explain how to avoid overdrafts and the significance of keeping track of their balance. Introduce them to how to access credit, and use it responsibly. Explain how credit cards work, the importance of paying off balances in full each month, when it’s okay to carry a balance, and the long-term benefits of building a positive credit history.

And let’s not forget your child’s new tax obligations. Teach them how to file taxes, what documents they need, and how to understand their W-2 forms, or what it means to be a 1099. Explain the importance of keeping accurate records and how to navigate basic tax software.

Health care is another critical area where your child needs education. Let your child know that you can’t make medical decisions for them and you won’t have access to their health records anymore – unless they give it to you. I’ll cover which essential documents they need in a minute, but first, let’s talk about the importance of communication in helping them document their wishes properly.

Strategy 2: Encourage Communication

Adulthood often involves having difficult conversations (as if I’m telling you anything you don’t know!). Two of those conversations to have with your child have to do with their healthcare and financial decisions in the event of an emergency.

First off, I want to say that even thinking about your child being in an emergency medical situation is hard to think about, much less talk about. And it will probably be much harder for you than it will be for them. It’s OK. Take a deep breath. You can do this!

After you’ve breathed your way to calm, have an open conversation about what your child would want to happen in various medical scenarios. If they became incapacitated, who would they want to make decisions on their behalf? Both parents or one of you first, then the other? Or do they want anyone else involved in the medical decisions, if they cannot make them on their own. Be open to the possibilities that they have other people in their life that they may want to include, and be glad they are telling you about it, if that’s the case.

Do they know what a ventilator is and whether they’d want one if it became an issue? What about a feeding or hydration tube? And what about resuscitation? It’s necessary to talk about these things so your child’s wishes are honored. Who would they want to have access to them, in case of an accident or an illness? Once you know the answers to these questions, you can help your child create a health care directive and medical power of attorney.

Have the same conversations about finances. Do you know which and how many financial accounts they have? If they’re in college, how will you access their account to stop tuition payments or housing payments if necessary? Will you be able to access their checking account if bills need to be paid? Your child may be reluctant to discuss these matters with you, but assure them you have no intent to violate their autonomy. You simply want to be there for them, if needed.

Strategy 3: Legal Planning

Once you and your child have had these difficult conversations, emphasize the need to get a legal plan in place so their wishes are documented and honored. At the least, your adult child’s legal plan should include the following documents:

Health Care Proxy and Advance Directive. A health care proxy grants someone, usually you, the authority to make medical decisions on your child’s behalf if they cannot. An Advance Directive complements this by outlining their medical treatment preferences in various scenarios, ensuring their wishes are respected even when they can’t voice them.

HIPAA Authorization. The HIPAA Authorization is equally important. HIPAA (Health Insurance Portability and Accountability Act) is designed to protect patient privacy, but it can also prevent you from accessing your child’s medical information without their explicit permission. By signing a HIPAA Authorization, your child can ensure that you can speak with doctors and receive updates on their condition.

Living Will. A Living Will is another important document to consider. This outlines your child’s wishes regarding end-of-life care, such as whether they want to receive life-sustaining treatments. Having these preferences documented can provide clarity and guidance during difficult times, ensuring that their wishes are honored.

Power of Attorney. A Power of Attorney allows your adult child to appoint someone (again, usually you) to manage their financial affairs if they are unable to do so. This can include everything from paying bills to managing bank accounts and handling investments. Without this document, you might find it difficult to step in and help when needed.

It may also be important for your adult child to have a plan in place for what happens after death. If that’s the case, they need a will or trust. Reach out to me and I can educate you and your child on whether post-death planning is needed at this stage in your child’s life.

Finally, life circumstances will change, so let your child know it’s important to review their documents regularly and update them as needed. Encourage your young adult to revisit their decisions periodically, especially if they experience significant life changes such as getting married, moving to a new state, or starting a new job. At my firm, constant contact is part of our process so our clients never have to remember on their own to update their plan. We do the remembering for you.

Your Next Step

Now that you are armed with 3 strategies for navigating your child’s transition into adulthood, your next step is to book an appointment with our firm so we can support you to have these conversations, and to get your child’s legal plan in place.

Now, before you go thinking that you don’t need an attorney and can use a cheap online tool, or even AI, I encourage you to think about what’s at stake. Your child’s health and well-being. Your child’s growth. The opportunity to teach your child about how to prioritize the things that matter most. When I work with you, one of the best things I can do is to get to know your children as they become adults. Ideally, it will be me (or my firm) that they’ll turn to for guidance throughout their lifetime, and to be there for them, when you can’t be. No cheap legal plan can do that.

The Support You and Your Child Need

As a Personal Family Lawyer Firm, we know that navigating the transition to adulthood can be challenging, both for you and your child. Understanding the legal changes that come with turning 18 and using the 3 legal documents (and the conversations that go with them) in this article can help you provide the support and guidance your child needs. But you don’t need to navigate this transition alone. We can educate you and your child about their new legal responsibilities, support you to have the hard conversations, and help your child put a legal plan in place.

Contact us to learn how our Life & Legacy Planning process supports your family to make the very best decisions about the things that matter most. Click here to schedule a 15-minute conversation.

This article is a service of a Personal Family Lawyer® Firm. We don’t just draft documents; we ensure you make informed and empowered decisions about life and death, for yourself and the people you love. That’s why we offer a Life & Legacy Planning Session™, during which you will get more financially organized than you’ve ever been before and make all the best choices for the people you love. You can begin by calling our office today to schedule a Life & Legacy Planning Session™.

The content is sourced from Personal Family Lawyer® for use by Personal Family Lawyer® firms, a source believed to be providing accurate information. This material was created for educational and informational purposes only and is not intended as ERISA, tax, legal, or investment advice. If you are seeking legal advice specific to your needs, such advice services must be obtained on your own separate from this educational material.

Proper estate planning can keep your family out of conflict, out of court, and out of the public eye. Are you ready to protect your loved ones and legacy? Check out my next presentation.

They’re Not Kids Anymore! Navigating Your Child’s Transition Into Adulthood

If you’re a father, you’ve always strived to provide the best for your family, ensuring their well-being and securing their future. However, even the most well-intentioned plans can falter if you overlook the complexities of estate planning. So this Father’s Day, let’s celebrate all of you dads and explore some common pitfalls that fathers often encounter, then offer practical strategies to navigate them successfully.

Heads up before we dive in; I’ll provide some stories below that illustrate what happens when a dad hasn’t created an estate plan or hasn’t updated it over time. The names of the people below are made up, but the scenarios I’ll describe are common.

Pitfall No. 1: Procrastination

If you’re a father, the weight of responsibility for your family’s well-being often rests heavily on your shoulders. However, even the most well-intentioned plans can fail if you overlook the complexities of estate planning. One of the most significant pitfalls is procrastination, or postponing the process under the assumption that you have ample time or that your assets are currently too modest to warrant formal planning. But the truth is that estate planning is crucial for individuals of all ages and asset levels! Unexpected events can occur at any time, leaving your loved ones in a bad situation if you haven’t properly documented your wishes.

Take for example, John, a 45-year-old father of three, who put off creating a will, thinking he had decades ahead of him. You can’t really blame him, can you? Many of us are in the same boat. However, he passed away tragically and unexpectedly, leaving his family to deal with his affairs in the court process called probate. The probate process was lengthy, and his assets were frozen and unavailable for his kids until the court process played out. In addition, probate drained his assets, so there wasn’t as much to leave his kids in the end.

I doubt this is what John would have wanted.

So dads, to avoid the procrastination trap, it’s essential to approach estate planning with a sense of urgency. Start the process as soon as possible, and review your plan regularly to ensure it remains aligned with your evolving circumstances and family dynamics (keep reading for more information on how I can help!).

Pitfall No. 2: Failing to Update Your Plan Over Time

This brings us to another pitfall: failing to update your plan after significant life events, such as marriages, divorces, births, or deaths. Life is inherently dynamic, and your estate plan should reflect those changes. Your plan should reflect your life as closely as possible, otherwise it could become ineffective or even invalid. And if that happens, you end up like John, even if you already have an estate plan.

Updating your estate plan over time is crucial. So make a habit of reviewing your plan at least every three years, preferably annually, or whenever a major life event occurs. When you work with me, I will help you ensure your plan accurately reflects your current wishes and aligns with any changes in state or federal laws.

Pitfall No. 3: Not Communicating With Loved Ones

Contrary to common belief, estate planning is not solely about legal documents, such as a Will, Trust or Power of Attorney. Documents are merely the byproduct of good estate planning. The real power of estate planning is in having open and honest communication with your loved ones. However, many fathers make the mistake of keeping their estate plans a closely guarded secret, leaving their families in the dark about their intentions and wishes. This lack of transparency can breed misunderstandings, conflicts, and resentments that can undermine the effectiveness of your plan and strain family relationships.

Let’s look at David’s story for a greater understanding. David, a successful business owner and loving father, always assumed his oldest son would take over the family business after his passing. So David’s estate plan included a provision wherein his oldest son inherited the business. When David died, however, his son revealed that he had different career aspirations and didn’t want to run the business. This led to family conflict – because David didn’t have a “Plan B” in his estate plan.

As a result, the family had to go to probate court, spending lots of time, energy, attention, and money, to get the business transferred to the one family member who wanted to run the business. Had David discussed his wishes openly, the family could have addressed their concerns together and arrived at a mutually agreeable solution that would have saved them the unnecessary hassle of probate court.

So what can you learn from David’s story? Share your wishes with your family members, explain your reasoning, and address any concerns they may have. This open dialogue can foster a deeper understanding and strengthen the bond between you and your loved ones. It also allows your loved ones to provide valuable insights and perspectives that can help refine and improve your plan. What a loving gift to give your family!

Pitfall No. 4: Not Working With a Professional

The last pitfall I’ll address is going at it alone, or doing your plan cheaply online. As I pointed out above, estate planning is not just about creating a few documents and putting them away on a shelf until something happens. There’s much more to it.

Instead, work closely with an estate planning firm like ours, who can help you craft a plan that fits your unique family dynamics, wishes and assets, as well as keep in touch over time to ensure your plan is updated and works when you need it to. At my firm, we support you with all this and more, including helping you structure your plan in a tax-efficient manner, minimizing the impact of taxes on your assets and ensuring your loved ones receive the maximum benefit from your estate.

I also help you address any unique circumstances within your family, such as a family business, a child with special needs or a family member with addiction issues, ensuring that your plan is tailored to meet the specific needs of your loved ones.

So dads, after reading this, I hope it’s clear that estate planning is a profound expression of your love and responsibility as a father. By taking action now, you can navigate the pitfalls and create a lasting legacy that transcends your lifetime. Remember, your knowledge and attention to detail today can shape the future of your loved ones for generations to come.

How We Support You to Avoid These Common Pitfalls

As a Personal Family Lawyer Firm, we understand that protecting your family goes far beyond just legal documentation. Our mission is to empower you to enshrine your hopes, values, and profound love for your children into a comprehensive plan that preserves your family’s integrity for generations to come. We take the time to truly understand what family means to you—the struggles you overcame, the values you hold dear, the future you envision. And then we help you craft a tailored estate plan that meets your needs and stays updated over time.

So this Father’s Day, give yourself and your children the greatest gift: your love. Book a call with our office to learn how we can support you, and by extension, your entire family. Simply click on this scheduling link.

This article is a service of a Personal Family Lawyer® Firm. We don’t just draft documents; we ensure you make informed and empowered decisions about life and death, for yourself and the people you love. That’s why we offer a Life & Legacy Planning Session™, during which you will get more financially organized than you’ve ever been before and make all the best choices for the people you love. You can begin by calling our office today to schedule a Life & Legacy Planning Session™.

The content is sourced from Personal Family Lawyer® for use by Personal Family Lawyer® firms, a source believed to be providing accurate information. This material was created for educational and informational purposes only and is not intended as ERISA, tax, legal, or investment advice. If you are seeking legal advice specific to your needs, such advice services must be obtained on your own separate from this educational material.

Proper estate planning can keep your family out of conflict, out of court, and out of the public eye. Are you ready to protect your loved ones and legacy? Check out my next presentation.

Father Knows Best: Avoiding Common Estate Planning Pitfalls

As an LGBTQIA+ non-biological parent, June’s arrival sparks a flurry of Pride celebrations reminding you of the remarkable progress the community has made, while also shining a light on the ongoing fight for full equality. One area where you may still face unique legal hurdles is in ensuring your parental rights are properly protected, if you are a non-biological parent. Marriage may not be enough, but marriage in conjunction with estate planning gives you the maximum peace of mind.

This Pride Month, take the time to safeguard your family’s future by putting the proper legal protections in place for yourself and the people you love. You worked hard to build this life —don’t let lack of planning put it all at risk. In this article, I’ll address some key actions to take so you’re empowered to advocate for your rights as an LGBTQIA+ non-biological parent.

Establish Legal Parentage

As a non-biological parent, your first priority is to ensure you are recognized as the legal parent of your child or children. This may seem like a given, but the laws around legal parentage can vary significantly between states and get tricky for LGBTQIA+ families.

For example, imagine your partner gives birth to a child through donor insemination, and you are not the biological parent. In many states, you would not automatically be considered a legal parent to that child—even if you’re married. The same applies to same-gender couples who have a child through surrogacy or adopt a child.

Without taking additional steps like a second-parent adoption or other legal processes, you could face an uphill battle asserting your parental rights and decision-making authority about the child’s care, education, and other crucial matters. This is the case even if you are co-parenting a child with your partner or spouse who is the biological parent of the child. It may sound extreme, but there are cases of non-legal LGBTQIA+ parents being denied the ability to make medical decisions for their own child or facing obstacles traveling across state lines together.

Build your family’s foundation on a rock, not sand. No matter how your child came into your lives, be sure to take the proper legal steps to ensure you have equal legal standing and rights as a parent, from day one.

Get Vital Legal Documents in Place

Beyond solidifying legal parentage, you need other legal documents in place to protect your role as a non-biological parent:

Medical Consent Forms. These forms explicitly authorize you to make medical decisions for your children in any situation. Without them, a hospital could potentially deny you the ability to consent to a life-saving procedure, if your legal status is called into question.

Parenting Agreement. If you’re not legally married to your co-parent, a formal parenting agreement is absolutely critical. This document outlines both party’s intentions, roles, responsibilities, and legal rights/expectations for raising the child. It can dictate factors like living arrangements, decision-making powers, financial obligations and more.

Without this agreement, a bitter break-up or disagreement could put your relationship with your child in legal jeopardy, especially if there isn’t an obvious framework for who has custodial rights. A thoroughly drafted parenting agreement acts as your concrete evidence of the intended family structure.

Wills and Guardianship. If the unthinkable happens and you (or your parenting partner) were to pass away, your children’s guardianship could potentially get caught up in legal battles with blood relatives who may not respect your family situation. The same goes for an unmarried co-parenting situation where your child’s other parent may not have automatic guardianship rights. Anytime you go to court, the potential for conflict increases exponentially. So do expenses. It’s always best to avoid the court process if at all possible (and here, it’s possible!).

This makes it absolutely imperative to explicitly document your choice of legal guardians for your children in case you are incapacitated or pass away. A Kid’s Protection Plan, where you nominate guardians for your children, exclude anyone you wouldn’t want, say what happens if they’re with a babysitter and you’re in an unforeseeable accident, prevents family you’d never want raising them from doing so, and ensures they’re never taken into the care of strangers, can not only help prevent ugly custody battles, but also make sure your kids are provided the love and stability they deserve.

As an LGBTQIA+ parents, these provisions are the way to reinforce your intentions and values about who should care for your children in keeping with the family structure you created. Don’t leave it up to a judge’s interpretation, who knows nothing about you and your children. Think about it: a judge is a complete stranger. Do you really want a complete stranger deciding what happens to your kids if you were no longer here? Of course not! So take action while you can, and if you are the non-biological parent in relationship with the biological parent, and without clear legal parentage, it’s even more critical – make sure your child’s biological parent has a Kids Protection Plan in place.

Build a Support System

Beyond legal documentation, it’s just as important to fortify your family with trusted allies and support networks who can advocate for your rights if they are ever challenged.

Look into connecting with local or national LGBTQIA+ family organizations and online communities where you can share advice and learn from others facing similar barriers. Groups like COLAGE (Children of Lesbians and Gays Everywhere) provide helpful resources.

You should also identify LGBTQIA+ friendly legal advisors, who will take a heart-centered approach to estate planning, and who really, really cares about your family. As a Personal Family Lawyer®, our firm will set you up with solid legal protections, and also be there for you and your family, anytime you need legal support in the future.

At the end of the day, the sad reality is that despite how far LGBTQIA+ rights have come, you may still face prejudiced individuals or institutions that try to undermine the legal protections you put in place. Having a solid support system in your corner could make all the difference.

Leave a Legacy, Not a Mess

As an LGBTQIA+ parent, you may have had to overcome many hurdles simply to become a parent to your child or children. Now it’s time to ensure you can leave the lasting legacy you envision for them.

With a comprehensive estate plan that works when you and your loved ones need it to, you can capture the immense love, sacrifice and life lessons that went into creating and nurturing your family unit. You can memorialize the values, heritage and core principles you hope to impart on your children and can outline cherished ceremonial traditions you want carried on at important milestones.

As a Personal Family Lawyer, we don’t just draft estate planning documents for you, but with our Life & Legacy Planning process, we ensure we create a plan that works for you when your family needs it, and that plan is maintained and updated over time. As a result, nothing that matters is lost, and you won’t leave a mess for the people you love.

On top of that, we don’t just ensure you pass on your money, but the intangible assets that truly matter to the people you love. During our Life & Legacy Planning process, we’ll record you speaking about what matters most for the people you love, creating a family heirloom that will be passed on for generations.

Get Support for the Journey

Even in 2024, the road to equality and respect is an ongoing battle for LGBTQIA+ parents and families. But you don’t have to figure it out alone. This Pride Month, connect with a Personal Family Lawyer who can empower you to protect your family structure and parental rights through comprehensive estate planning.

Estate planning is not just about legal formalities, but ensuring your lifetime of efforts to create your family leaves a proud, enduring legacy for generations to come. With the proper guidance, you can celebrate future Pride events confident your journey won’t be derailed by preventable legal oversights. The peace of mind of knowing you’ve shored up your family’s legal standing is one of the greatest acts of love you can provide. It’s not only a gift of love for your children, but a gift of love to yourself.

How We Support You to Protect Your Family

As a Personal Family Lawyer Firm, we understand that protecting your family goes far beyond just legal documentation. Our mission is to empower you to enshrine your hopes, values and profound love for your children into a comprehensive plan that preserves your family’s integrity for generations to come. We take the time to truly understand what family unity means to you—the struggles you overcame, the values you hold dear, the future you envision. And then we help you craft a tailored estate plan that meets your needs.

This Pride Month, give yourself and your children the greatest gift: a lasting celebration of your family’s identity, equality and unbreakable bonds.

Schedule a complimentary 15-minute call with our office to learn more.

This article is a service of a Personal Family Lawyer® Firm. We don’t just draft documents; we ensure you make informed and empowered decisions about life and death, for yourself and the people you love. That’s why we offer a Life & Legacy Planning Session™, during which you will get more financially organized than you’ve ever been before and make all the best choices for the people you love. You can begin by calling our office today to schedule a Life & Legacy Planning Session™.

The content is sourced from Personal Family Lawyer® for use by Personal Family Lawyer® firms, a source believed to be providing accurate information. This material was created for educational and informational purposes only and is not intended as ERISA, tax, legal, or investment advice. If you are seeking legal advice specific to your needs, such advice services must be obtained on your own separate from this educational material.

Proper estate planning can keep your family out of conflict, out of court, and out of the public eye. Are you ready to protect your loved ones and legacy? Check out my next presentation.

Protecting Your LGBTQIA+ Family: A Pride Month Guide to Estate Planning for Non-Biological Parents

Memorial Day brings with it an opportunity to reflect on the concepts of mortality, remembrance, and legacy. As we remember the brave men and women who lost their lives serving in the military, may this day also inspire you to think about the legacy you wish to leave behind.

But, first, what is a legacy, really? “Legacy” is often misunderstood and so is estate planning. Legacy and estate planning are often perceived as “only for the wealthy” and/or “philanthropic”. But that couldn’t be further from the truth.

Legacy isn’t just about money or wealth. As my mentor Ali Katz says: “Legacy is the choices you make now, the actions you take now, the way of being you are now, and the ripple of impact beyond your lifetime.”

Legacy includes capturing your life stories, passing on your values, and ensuring your loved ones have a record of the essence of what matters to you. These are the things you leave behind that mean the most to your loved ones. Money can’t even compare. Thinking of it this way, it’s easy to see that every human has a legacy to create and leave behind, including you!

Estate planning, on the other hand, is something many people think they understand, but really don’t. It isn’t just about getting your Will done, or documenting what your end-of-life health care wishes are. Estate planning, like legacy, encompasses much more. It’s not about getting some documents signed. Estate planning is the vehicle that allows you to leave a legacy.

So let’s dive in for more understanding on what “legacy” really means and how you can secure your legacy for the benefit of your loved ones.

Understanding What Legacy Truly Is

Legacy, at its core, is about connecting the generations, and Life & Legacy Planning is the way to do it. Here’s an example. Consider a teacher who has spent her career fostering curiosity and resilience in her students. She may not have millions of dollars to give away, but she can use her estate plan to leave her personal library to a local school. She may even set up a small scholarship fund in her estate plan so she can continue supporting education long after she’s gone. And, if she has children or close friends she cooks for regularly, she may leave a book full of her recipes they all love.

Her legacy then becomes not just about the resources she left behind, but about inspiring future generations to value learning and perseverance, and nourishment. Similarly, your estate plan can be crafted to perpetuate the principles you deem most important, making your influence felt well into the future.

So now, take a minute to reflect. What principles are most important to you? How do you want to use them to connect your generation to the next?

Estate Planning as a Form of Love

In emphasizing the value of estate planning as the vehicle that allows you to leave a legacy, know that estate planning should be tailored for each person, each person’s family dynamics, and each person’s values. No two people are the same, no two families are the same, and therefore, no two estate plans should be the same. This personal touch transforms estate planning from a mundane task, that most people put off because they don’t see the value, into a powerful act of love.

Proper and customized estate planning can also alleviate the potential for family conflict, which oftentimes results in irretrievably broken family relationships. But when you use estate planning as a vehicle for securing your legacy, it has the power to preserve these relationships and uphold family harmony. Estate planning is then transformed into an enduring gesture of care and love.

Consider as an example a devoted husband and father who deeply valued his family’s annual summer retreats to a beloved lakeside cabin. Understanding the special place the cabin held in his and his family’s hearts, he specifically detailed in his Will his wish for the property to remain in the family, passing down to his children and grandchildren.

He also set up a small fund to cover the cabin’s upkeep, ensuring that his family would continue to enjoy it without financial burden. In doing so, this loving husband and father not only preserved a cherished family tradition but also created a physical space for remembrance and togetherness, allowing future generations to share in the joy and serenity he found there. This thoughtful element of his estate plan demonstrates how such preparations are acts of love, weaving his memory and values into the fabric of his family’s future.

Take another minute to reflect. How would you craft your own legacy into a plan of action?

Practical Steps to Create Your Legacy

Taking the first step in estate planning can feel daunting, but when you frame it as an act of love and legacy preservation, it becomes a deeply meaningful process. Start by identifying what matters most to you. This could be family traditions, a commitment to charity, a passion for art, or anything else that defines your personal story and values. Begin by listing these priorities and considering how they can be integrated into your estate plan.

Next, consult with a Personal Family Lawyer (“PFL”) who understands the intersection of legacy and estate planning through a special process called Life & Legacy Planning. A PFL will help you get clear on your values and goals, then together, you’ll create a customized plan that fits you and honors the legacy you wish to leave behind. For instance, if you, like the devoted father in the example above, have a cherished family property, a PFL can advise you on how to set up a trust to manage that property and stipulate how it should be maintained and used by future generations.

A PFL will also record a Life & Legacy Interview that your family will cherish for years. The Interview allows you to express your love, hopes, and reasons behind your decisions and is a comforting and clarifying piece for your loved ones, ensuring they understand your intentions and feel your presence in the provisions you’ve made. You can even record messages to send to beneficiaries that provide stories and details about a special possession or heirloom and why you chose to give it to them.

By taking these steps, you’re not just planning for the future; you’re crafting a legacy that carries your values and love forward, ensuring that your impact on the world persists and that your memory continues to serve as a source of inspiration and unity for those you hold dear.

Memorial Day Is an Opportunity for Action

This Memorial Day, as you reflect on the sacrifices of those who gave their all (and what a legacy that is!), take action to get your estate plan in place. Remember, estate planning is not just for the wealthy; it is for everyone. It’s about making your mark, much like the soldiers we honor, whose legacies are remembered for generations.

So let this Memorial Day be the catalyst for you to start or update your estate plan. In doing so, you honor your life and ensure connection among the generations. Just as we come together as a nation to remember, let’s also take steps to put our love into action.

How We Can Help You Take Action Today

As a Personal Family Lawyer Firm, we don’t merely dispense legal counsel; we empower you to reflect on how you want to be remembered and how you want to pass on the values you hold dear. We take the time to fully understand what’s important to you, and then together, we’ll craft a thoughtful and holistic plan that results in the greatest gift you can leave your loved ones: your love.

To learn more about how we approach estate planning as the intersection of love and legacy, schedule a complimentary 15-minute call with our office.

This article is a service of a Personal Family Lawyer® Firm. We don’t just draft documents; we ensure you make informed and empowered decisions about life and death, for yourself and the people you love. That’s why we offer a Life & Legacy Planning Session™, during which you will get more financially organized than you’ve ever been before and make all the best choices for the people you love. You can begin by calling our office today to schedule a Life & Legacy Planning Session™.

The content is sourced from Personal Family Lawyer® for use by Personal Family Lawyer® firms, a source believed to be providing accurate information. This material was created for educational and informational purposes only and is not intended as ERISA, tax, legal, or investment advice. If you are seeking legal advice specific to your needs, such advice services must be obtained on your own separate from this educational material.

Proper estate planning can keep your family out of conflict, out of court, and out of the public eye. Are you ready to protect your loved ones and legacy? Check out my next presentation.

Memorial Day Reflections: Crafting Your Lasting Legacy With Estate Planning

Welcome back to our discussion on securing a comfortable retirement! In the first part of this series, we explored essential steps including estate planning, preparing for long-term care, and passing on your legacy. As we continue with the second part of our series, we’ll delve into additional areas that are crucial for ensuring your golden years are not only financially stable but also enriched with independence, health, and continued personal growth. So let’s pick up where we left off.

Step 6: Consider Your Housing Needs

Why It’s Important: Adapting your living environment to meet your changing mobility and health needs can enhance your independence and quality of life (and who doesn’t want that?!). As physical abilities change with age, a home that accommodates these changes can help maintain a higher level of independence, reduce the risk of accidents, and potentially delay or avoid the need for an assisted living facility. Moreover, comfortable and accessible living conditions contribute significantly to happiness and well-being in your later years.

Practical Steps:

Assess Home Accessibility: Evaluate your home for potential mobility issues and consider modifications like ramps, wider doorways, or bathroom grab bars.

Explore Senior-Friendly Housing Options: If extensive modifications are too costly or impractical, consider moving to a senior-friendly community that offers additional amenities and services.

Find a Personal Family Lawyer in Your Community Who Offers Elder Care Planning. A Personal Family Lawyer (“PFL”) who offers elder care planning can help you navigate your options and create a plan that preserves your assets for your loved ones, rather than draining them for housing and health care costs. Go to personalfamilylawyer.com to find the nearest PFL who offers elder care planning and make an appointment on their website. Many PFLs have virtual offices for your convenience, so if there isn’t a PFL listed in your locality, choose the closest one.

Step 7: Embrace Technology for Independence

Why It’s Important: Modern technology can significantly improve the convenience and safety of daily life for seniors. Technologies that assist with daily tasks can extend independence, reduce caregiver burden, and enhance your overall quality of life. Additionally, health-monitoring technologies can alert caregivers and medical professionals to potential health issues before they become severe, ensuring timely medical intervention.

Practical Steps:

Consult with a PFL and Join Their PFL FamilyCare Program. A PFL who has a FamilyCare Program in place has, as one of the benefits of membership, a subscription to a secure, online system that houses your important legal and health care documents so they’re immediately available to doctors, hospitals, and caregivers. This is really important! Most people who have estate plans with health care documents have them stored on a shelf and aren’t accessible when they need them. That’s no good in the event of an emergency. But a PFL has your back.

Health Monitoring Technologies: Employ devices that can monitor vital signs and remind you to take medications. Your doctor may be able to help with this.

Consider Using Smart Home Devices: You can automate lighting, heating, and security to manage your home environment easily. If you aren’t technologically savvy, ask a younger family member to help. Gen Z can figure that out in a heartbeat!

Step 8: Stay Active and Engaged

Why It’s Important: Active engagement in physical, social, and mental activities can significantly enhance your quality of life and health in retirement. Maintaining an active lifestyle helps prevent common age-related health problems, improves mental health, and provides valuable social interactions that can combat loneliness and depression. When you engage in a variety of activities you also keep your mind sharp and gain a sense of accomplishment and happiness.

Practical Steps:

Join Community Groups or Clubs: Engage in activities that match your interests, such as book clubs, gardening, or volunteering. If you’re active on Facebook, you can find groups there that meet in your local community. Joining online groups counts too!

Regular Exercise: Participate in senior-friendly exercise programs to maintain health and mobility.

Pursue New Learning Opportunities: Consider taking classes at local community colleges or online to keep your mind sharp and learn new skills.

Step 9: Develop a Sustainable Retirement Budget

Why It’s Important: A well-planned budget is crucial to ensure that your savings last throughout your retirement years. A sustainable budget helps you manage your finances effectively, avoiding overspending and ensuring that you have funds available for unexpected expenses. A good budgeting practice can also help you maintain a comfortable lifestyle while safeguarding against market volatility and economic downturns.

Practical Steps:

Identify Essential vs. Non-Essential Expenses: Consider making adjustments to your spending habits if needed to ensure you can cover necessary costs while still enjoying your retirement.

Plan for Unexpected Costs: Include a buffer in your budget for unforeseen expenses to avoid financial strain.

Consult with a PFL. A PFL, as part of their unique PFL Life & Legacy Planning process, will help you get more financially organized than you’ve ever been before. Together, you’ll create a complete asset inventory (we call it a “personal resource map”, so you know exactly what you have and how long it will last. The inventory also ensures that your loved ones will be able to find your assets after you’re gone, so nothing is lost to the government. Check out your State’s Department of Unclaimed Property website and prepare to be shocked to see how much money has been lost! Traditional estate planning attorneys will not help you, but a PFL includes the inventory as part of every estate plan.

Step 10: Review and Adjust Your Estate Plan Regularly

Why It’s Important: Life changes, and so should your estate plan to ensure it continues to meet your evolving needs and circumstances. Regular reviews ensure your plan works when you and your family need it to, keeping them out of court and conflict after you’re gone. If your estate plan is current with the ever-changing estate and tax laws, chances are it will work and your wishes will be honored if you become incapacitated or when you die.

Practical Steps:

Work With a PFL and Join Their PFL FamilyCare Program. All PFLs have, as part of the Life & Legacy Planning process, a built-in cadence of reviewing your plan every 3 years at no charge. However, if your PFL has a FamilyCare Program in place, join and you’ll receive an annual review at no cost. You’ll also receive membership benefits that include special, members-only pricing for updates to your plan.

Regular Financial Reviews: As part of the PFL FamilyCare program, your PFL will also review your asset inventory annually so that it stays up to date. This ensures your family will receive your assets, not the government. If your PFL does not have a FamilyCare Program yet, they will review your asset inventory every 3 years with you.

And now we’ve come to the end of our 2-part series on how to enjoy your retirement with ease and peace of mind. I hope you’ve found this information helpful and inspired you to take action right away because what matters most to me is your ability to live a fulfilling life and give your loved ones a legacy they will treasure.

We Can Help Secure Comfort in Your Retirement

At our firm, we do more than just assist with your immediate retirement planning needs; we ensure that your future is as vibrant and secure as possible. The intricacies of adapting your living space, integrating modern technology for better health and independence, staying socially and physically active, and managing your finances can make retirement seem overwhelming. As your Personal Family Lawyer Firm, we simplify these aspects and tailor solutions to fit your lifestyle and aspirations, all within your time and budget.

If you want to explore how we can help you develop a retirement plan that not only safeguards your finances but also enriches your daily life, we encourage you to book a complimentary 15-minute call with us. Together, let’s make your retirement years as fulfilling and carefree as possible.

This article is a service of a Personal Family Lawyer® Firm. We don’t just draft documents; we ensure you make informed and empowered decisions about life and death, for yourself and the people you love. That’s why we offer a Life & Legacy Planning Session™, during which you will get more financially organized than you’ve ever been before and make all the best choices for the people you love. You can begin by calling our office today to schedule a Life & Legacy Planning Session™.

The content is sourced from Personal Family Lawyer® for use by Personal Family Lawyer® firms, a source believed to be providing accurate information. This material was created for educational and informational purposes only and is not intended as ERISA, tax, legal, or investment advice. If you are seeking legal advice specific to your needs, such advice services must be obtained on your own separate from this educational material.

Proper estate planning can keep your family out of conflict, out of court, and out of the public eye. Are you ready to protect your loved ones and legacy? Check out my next presentation.

10 Steps to Take Now to Secure a Comfortable Retirement: Part 2

Retirement is more than just an end to the working years; it’s an exciting new phase of life that requires thoughtful preparation and strategic planning. Since May is Older Americans Awareness Month, it’s the perfect opportunity to explore 10 steps you can take now to ensure a comfortable and fulfilling retirement. In this article, we’ll discuss the first 5 steps, why they’re important, and how to implement them. Next week, we’ll continue with the remaining 5 steps.

Let’s dive in, shall we?

Step 1: Plan for the Transfer of Your Assets

Why It’s Important: Effective estate planning ensures that your assets are distributed according to your wishes, potentially reduces estate taxes, and can prevent a lot of legal complications for your heirs. Proper estate planning also helps to avoid the public, often lengthy and costly process of probate, ensuring that your heirs have quicker access to the assets you leave behind. Moreover, clear directives in estate planning can prevent family disputes (sometimes resulting in irretrievably broken relationships) and ensure that your specific instructions are followed, preserving your legacy exactly as you intend.

Practical Steps: Consult with a Personal Family Lawyer. A Personal Family Lawyer (“PFL”) always starts the client relationship with education about your options that align with your specific family dynamics, assets and wishes. From there, your PFL will help you create a tailored Life & Legacy plan that works when you and your family need it to, keeping you and them out of court and conflict. Importantly, a PFL can also help you avoid unnecessary taxes before and during retirement (and who doesn’t want that?).

Life Insurance: Having adequate coverage to handle any debts and funeral expenses can provide a financial cushion for those who depend on you. As part of the PFL Life & Legacy Planning process, your PFL can educate you about how much insurance you need and how to pass the funds to the people you want, while avoiding unnecessary taxes and ensuring the funds are available as soon as possible.